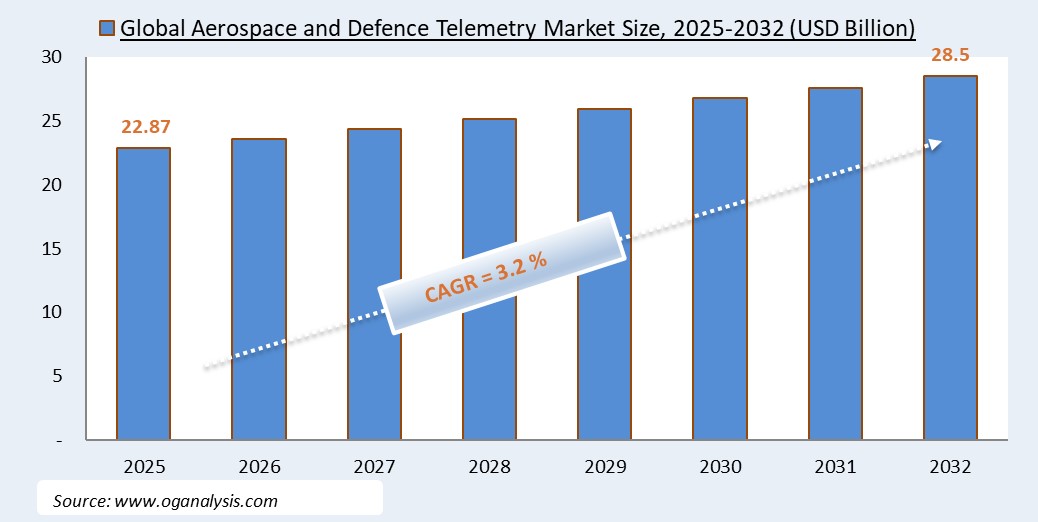

"The Global Aerospace and Defence Telemetry Market Size was valued at USD 22.87 Billion in 2025. Worldwide sales of Aerospace and Defence Telemetry Market are expected to grow at a significant CAGR of 3.2%, reaching USD 28.51 Billion by the end of the forecast period in 2032."

Aerospace and Defence Telemetry Market Overview

The aerospace and defense telemetry market plays a crucial role in ensuring real-time data acquisition, transmission, and analysis for military, space, and aviation applications. Telemetry systems are integral to monitoring the performance of aircraft, missiles, satellites, and unmanned aerial vehicles (UAVs), providing mission-critical insights that enhance operational efficiency and safety. The growing adoption of advanced communication technologies, including secure data transmission protocols and satellite telemetry, has expanded the scope of applications within this market. Governments and defense organizations worldwide continue to invest heavily in telemetry solutions to support space exploration, missile testing, and battlefield surveillance. Moreover, increasing geopolitical tensions and the rising demand for unmanned systems have driven the adoption of sophisticated telemetry networks. With rapid technological advancements in encryption, real-time analytics, and artificial intelligence integration, the market is witnessing a shift towards smarter and more resilient telemetry solutions that can withstand cyber threats and operate in contested environments.

In 2024, the aerospace and defense telemetry market has experienced significant technological innovations and strategic collaborations. The growing reliance on advanced satellite networks for secure and long-range data transmission has led to an increased demand for space-based telemetry solutions. Governments are enhancing their military capabilities by deploying telemetry-enabled missile systems and UAVs equipped with real-time communication modules for intelligence, surveillance, and reconnaissance (ISR) missions. Additionally, defense agencies are investing in next-generation telemetry infrastructure to support hypersonic missile testing, a key area of development among major military powers. The integration of cloud computing and AI-driven analytics in telemetry systems has enabled faster decision-making and enhanced situational awareness for defense operations. Furthermore, aerospace manufacturers are incorporating telemetry solutions into commercial aircraft to improve maintenance efficiency, enhance flight safety, and optimize fuel consumption. Amidst rising cybersecurity concerns, telemetry providers are implementing robust encryption technologies to ensure data security and prevent unauthorized access to sensitive defense communications.

Looking ahead to 2025 and beyond, the aerospace and defense telemetry market is poised for further transformation driven by advancements in quantum communication, software-defined radios, and 5G-enabled telemetry networks. The development of autonomous aerial and space-based systems will require highly sophisticated telemetry solutions capable of handling massive data loads in real time. Governments and space agencies are expected to increase their investments in deep space telemetry for interplanetary missions, further expanding the market's scope. The rise of network-centric warfare and digital battlefields will fuel demand for telemetry systems that offer seamless integration with command-and-control networks, enhancing operational capabilities for defense forces. Additionally, the proliferation of low-earth orbit (LEO) satellite constellations will facilitate real-time data relay for both military and commercial aerospace applications. Sustainability concerns will drive innovations in energy-efficient telemetry hardware, with manufacturers focusing on lightweight, high-performance components. As cybersecurity threats evolve, telemetry providers will continue refining encryption protocols and blockchain-based security measures to protect mission-critical defense communications, ensuring the long-term growth of this dynamic market.

Market Segmentation

- By Component:

- Telemetry Transmitters

- Receivers

- Antennas

- Sensors

- Data Acquisition Systems

- By Technology:

- Wired Telemetry

- Wireless Telemetry

- Satellite Telemetry

- By Application:

- Missile Guidance and Testing

- Flight Testing

- Space Exploration

- Unmanned Aerial Vehicles (UAVs)

- Military and Defense Operations

- By End-User:

- Defense Agencies

- Space Agencies

- Aerospace Manufacturers

- Commercial Airlines

- Research Institutions

- By Geography:

- North America (U.S., Canada, Mexico)

- Europe (U.K., Germany, France, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, South Korea, Rest of Asia-Pacific)

- Latin America (Brazil, Argentina, Rest of Latin America)

- Middle East & Africa (GCC, Israel, South Africa, Rest of MEA)

Major Players in the Aerospace and Defence Telemetry Market

- BAE Systems plc

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- Honeywell International Inc.

- Thales Group

- General Dynamics Corporation

- Safran S.A.

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Kratos Defense & Security Solutions, Inc.

- Teledyne Technologies Incorporated

- Curtiss-Wright Corporation

- Rohde & Schwarz GmbH & Co. KG

- Israel Aerospace Industries Ltd.

1. Table of Contents

1.1 List of Tables

1.2 List of Figures

2. Aerospace and Defence Telemetry Market Latest Trends, Drivers and Challenges, 2024 - 2032

2.1 Aerospace and Defence Telemetry Market Overview

2.2 Market Strategies of Leading Aerospace and Defence Telemetry Companies

2.3 Aerospace and Defence Telemetry Market Insights, 2024 - 2032

2.3.1 Leading Aerospace and Defence Telemetry Types, 2024 - 2032

2.3.2 Leading Aerospace and Defence Telemetry End-User industries, 2024 - 2032

2.3.3 Fast-Growing countries for Aerospace and Defence Telemetry sales, 2024 - 2032

2.4 Aerospace and Defence Telemetry Market Drivers and Restraints

2.4.1 Aerospace and Defence Telemetry Demand Drivers to 2032

2.4.2 Aerospace and Defence Telemetry Challenges to 2032

2.5 Aerospace and Defence Telemetry Market- Five Forces Analysis

2.5.1 Aerospace and Defence Telemetry Industry Attractiveness Index, 2024

2.5.2 Threat of New Entrants

2.5.3 Bargaining Power of Suppliers

2.5.4 Bargaining Power of Buyers

2.5.5 Intensity of Competitive Rivalry

2.5.6 Threat of Substitutes

3. Global Aerospace and Defence Telemetry Market Value, Market Share, and Forecast to 2032

3.1 Global Aerospace and Defence Telemetry Market Overview, 2024

3.2 Global Aerospace and Defence Telemetry Market Revenue and Forecast, 2024 - 2032 (US$ Million)

3.3 Global Aerospace and Defence Telemetry Market Size and Share Outlook By Component, 2024 - 2032

3.3.1 Telemetry Transmitters

3.3.2 Receivers

3.3.3 Antennas

3.3.4 Sensors

3.3.5 Data Acquisition Systems

3.4 Global Aerospace and Defence Telemetry Market Size and Share Outlook By Technology, 2024 - 2032

3.4.1 Wired Telemetry

3.4.2 Wireless Telemetry

3.4.3 Satellite Telemetry

3.5 Global Aerospace and Defence Telemetry Market Size and Share Outlook By Application, 2024 - 2032

3.5.1 Missile Guidance and Testing

3.5.2 Flight Testing

3.5.3 Space Exploration

3.5.4 Unmanned Aerial Vehicles (UAVs)

3.5.5 Military and Defense Operations

3.6 Global Aerospace and Defence Telemetry Market Size and Share Outlook By End-User, 2024 - 2032

3.6.1 Defense Agencies

3.6.2 Space Agencies

3.6.3 Aerospace Manufacturers

3.6.4 Commercial Airlines

3.6.5 Research Institutions

3.7 Global Aerospace and Defence Telemetry Market Size and Share Outlook by Region, 2024 - 2032

4. Asia Pacific Aerospace and Defence Telemetry Market Value, Market Share and Forecast to 2032

4.1 Asia Pacific Aerospace and Defence Telemetry Market Overview, 2024

4.2 Asia Pacific Aerospace and Defence Telemetry Market Revenue and Forecast, 2024 - 2032 (US$ Million)

4.3 Asia Pacific Aerospace and Defence Telemetry Market Size and Share Outlook By Component, 2024 - 2032

4.4 Asia Pacific Aerospace and Defence Telemetry Market Size and Share Outlook By Technology, 2024 - 2032

4.5 Asia Pacific Aerospace and Defence Telemetry Market Size and Share Outlook By Application, 2024 - 2032

4.6 Asia Pacific Aerospace and Defence Telemetry Market Size and Share Outlook By End-User, 2024 - 2032

4.7 Asia Pacific Aerospace and Defence Telemetry Market Size and Share Outlook by Country, 2024 - 2032

4.8 Key Companies in Asia Pacific Aerospace and Defence Telemetry Market

5. Europe Aerospace and Defence Telemetry Market Value, Market Share, and Forecast to 2032

5.1 Europe Aerospace and Defence Telemetry Market Overview, 2024

5.2 Europe Aerospace and Defence Telemetry Market Revenue and Forecast, 2024 - 2032 (US$ Million)

5.3 Europe Aerospace and Defence Telemetry Market Size and Share Outlook By Component, 2024 - 2032

5.4 Europe Aerospace and Defence Telemetry Market Size and Share Outlook By Technology, 2024 - 2032

5.5 Europe Aerospace and Defence Telemetry Market Size and Share Outlook By Application, 2024 - 2032

5.6 Europe Aerospace and Defence Telemetry Market Size and Share Outlook By End-User, 2024 - 2032

5.7 Europe Aerospace and Defence Telemetry Market Size and Share Outlook by Country, 2024 - 2032

5.8 Key Companies in Europe Aerospace and Defence Telemetry Market

6. North America Aerospace and Defence Telemetry Market Value, Market Share and Forecast to 2032

6.1 North America Aerospace and Defence Telemetry Market Overview, 2024

6.2 North America Aerospace and Defence Telemetry Market Revenue and Forecast, 2024 - 2032 (US$ Million)

6.3 North America Aerospace and Defence Telemetry Market Size and Share Outlook By Component, 2024 - 2032

6.4 North America Aerospace and Defence Telemetry Market Size and Share Outlook By Technology, 2024 - 2032

6.5 North America Aerospace and Defence Telemetry Market Size and Share Outlook By Application, 2024 - 2032

6.6 North America Aerospace and Defence Telemetry Market Size and Share Outlook By End-User, 2024 - 2032

6.7 North America Aerospace and Defence Telemetry Market Size and Share Outlook by Country, 2024 - 2032

6.8 Key Companies in North America Aerospace and Defence Telemetry Market

7. South and Central America Aerospace and Defence Telemetry Market Value, Market Share and Forecast to 2032

7.1 South and Central America Aerospace and Defence Telemetry Market Overview, 2024

7.2 South and Central America Aerospace and Defence Telemetry Market Revenue and Forecast, 2024 - 2032 (US$ Million)

7.3 South and Central America Aerospace and Defence Telemetry Market Size and Share Outlook By Component, 2024 - 2032

7.4 South and Central America Aerospace and Defence Telemetry Market Size and Share Outlook By Technology, 2024 - 2032

7.5 South and Central America Aerospace and Defence Telemetry Market Size and Share Outlook By Application, 2024 - 2032

7.6 South and Central America Aerospace and Defence Telemetry Market Size and Share Outlook By End-User, 2024 - 2032

7.7 South and Central America Aerospace and Defence Telemetry Market Size and Share Outlook by Country, 2024 - 2032

7.8 Key Companies in South and Central America Aerospace and Defence Telemetry Market

8. Middle East Africa Aerospace and Defence Telemetry Market Value, Market Share and Forecast to 2032

8.1 Middle East Africa Aerospace and Defence Telemetry Market Overview, 2024

8.2 Middle East and Africa Aerospace and Defence Telemetry Market Revenue and Forecast, 2024 - 2032 (US$ Million)

8.3 Middle East Africa Aerospace and Defence Telemetry Market Size and Share Outlook By Component, 2024 - 2032

8.4 Middle East Africa Aerospace and Defence Telemetry Market Size and Share Outlook By Technology, 2024 - 2032

8.5 Middle East Africa Aerospace and Defence Telemetry Market Size and Share Outlook By Application, 2024 - 2032

8.6 Middle East Africa Aerospace and Defence Telemetry Market Size and Share Outlook By End-User, 2024 - 2032

8.7 Middle East Africa Aerospace and Defence Telemetry Market Size and Share Outlook by Country, 2024 - 2032

8.8 Key Companies in Middle East Africa Aerospace and Defence Telemetry Market

9. Aerospace and Defence Telemetry Market Structure

9.1 Key Players

9.2 Aerospace and Defence Telemetry Companies - Key Strategies and Financial Analysis

9.2.1 Snapshot

9.2.3 Business Description

9.2.4 Products and Services

9.2.5 Financial Analysis

10. Aerospace and Defence Telemetry Industry Recent Developments

11 Appendix

11.1 Publisher Expertise

11.2 Research Methodology

11.3 Annual Subscription Plans

11.4 Contact Information

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Global Aerospace and Defence Telemetry Market is estimated to generate USD 22.87 Billion revenue in 2025.

The Global Aerospace and Defence Telemetry Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.2% during the forecast period from 2025 to 2032.

By 2032, the Aerospace and Defence Telemetry Market is estimated to account for USD 28.51 Billion.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!