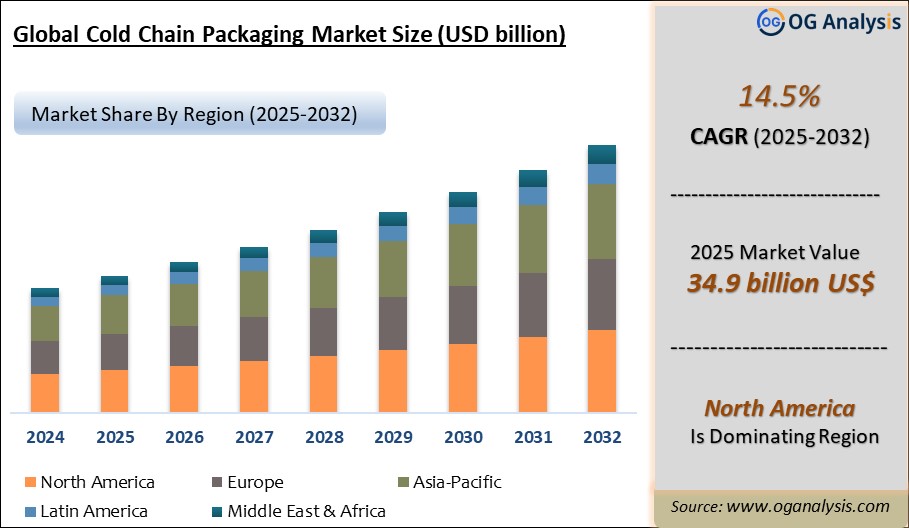

"The Global Cold Chain Packaging Market is valued at USD 31.0 billion in 2024 and is projected to reach USD 34.9 billion in 2025. Worldwide sales of Cold Chain Packaging are expected to grow at a significant CAGR of 14.5%, reaching USD 121.4 billion by the end of the forecast period in 2034."

The Cold Chain Packaging Market plays a critical role in maintaining the safety, quality, and efficacy of temperature-sensitive products across pharmaceuticals, food & beverages, and chemical sectors. With rising global demand for perishable goods, especially biologics, frozen food, and fresh produce, the need for efficient cold chain packaging solutions has surged. Technological innovations in insulation, phase change materials, and smart tracking systems are driving product evolution, while sustainability regulations are encouraging the shift toward recyclable and reusable materials. The growing penetration of e-commerce in the food and healthcare sectors is further propelling the market, making reliable last-mile cold chain logistics essential. Major companies are investing in smart packaging technologies to enhance temperature monitoring, minimize spoilage, and reduce logistics costs.

The market's expansion is supported by stringent international regulations governing temperature-sensitive goods and the increasing globalization of pharmaceutical and food supply chains. The rise of biologic drugs, vaccines, and precision medicine further elevates the importance of secure cold chain packaging. Emerging economies, particularly in Asia-Pacific and Latin America, present high-growth potential due to expanding healthcare infrastructure and demand for processed frozen foods. Companies are also focusing on lightweight and energy-efficient packaging to lower environmental footprints and shipping costs. The competitive landscape includes packaging material suppliers, container manufacturers, and third-party logistics providers offering integrated cold chain solutions.

Among product types, EPS containers represent the largest segment due to their widespread use in food and pharmaceutical logistics, offering excellent insulation at a lower cost compared to alternatives. Their lightweight structure and reliable thermal protection make them a preferred choice for large-scale cold shipments.

For end users, pharmaceutical packaging is the fastest growing segment, driven by the stringent temperature requirements of biologics, vaccines, and specialty medicines. Rising global demand for temperature-sensitive pharmaceuticals continues to boost the adoption of advanced cold chain packaging solutions in this segment.

Key Insights

The pharmaceutical sector is a major driver, with demand for temperature-controlled packaging rising due to vaccines, biologics, and personalized medicine requiring precise thermal regulation throughout transport.

Adoption of reusable cold chain packaging systems is increasing as companies seek sustainable and cost-effective alternatives to single-use solutions, reducing waste and lowering total cost of ownership.

Advanced phase change materials (PCMs) and vacuum insulated panels (VIPs) are enhancing performance in high-risk temperature excursions and long-distance cold transport scenarios.

Food and beverage segment sees strong growth in frozen, chilled, and ready-to-eat meals, especially with the expansion of online grocery delivery services requiring temperature consistency.

IoT-enabled cold chain packaging with real-time temperature, humidity, and shock monitoring is gaining popularity for its ability to prevent product losses and ensure regulatory compliance.

Asia-Pacific emerges as a rapidly growing regional market driven by increasing urbanization, dietary shifts, pharmaceutical demand, and infrastructure development in countries like India and China.

Logistics and transport firms are partnering with packaging solution providers to offer end-to-end cold chain services, combining container technology with advanced monitoring and handling protocols.

Innovation in materials such as biodegradable insulation foams and recyclable liners is gaining traction amid increasing pressure from governments and retailers for eco-friendly solutions.

Stricter regulations from agencies such as FDA, EMA, and WHO for drug safety are compelling pharmaceutical companies to invest heavily in validated and GDP-compliant cold chain packaging systems.

COVID-19 accelerated market development, particularly with the mass distribution of temperature-sensitive vaccines, establishing long-term investment trends in cold chain infrastructure and packaging.

Reort Scope

| Parameter | Detail |

|---|---|

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By End User, |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10 % free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Market Segmentation

By Product Type

- EPS Containers

- PUR Containers

- Pallet Shippers

- Vacuum Insulated Panels

- Others

By End User

- Food Packaging

- Healthcare Packaging

- Pharmaceutical packaging

- Industrial Applications

- Other

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

What You Receive

• Global Cold Chain Packaging market size and growth projections (CAGR), 2024- 2034• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Cold Chain Packaging.

• Cold Chain Packaging market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Cold Chain Packaging market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Cold Chain Packaging market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Cold Chain Packaging market, Cold Chain Packaging supply chain analysis.

• Cold Chain Packaging trade analysis, Cold Chain Packaging market price analysis, Cold Chain Packaging Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Cold Chain Packaging market news and developments.

The Cold Chain Packaging Market international scenario is well established in the report with separate chapters on North America Cold Chain Packaging Market, Europe Cold Chain Packaging Market, Asia-Pacific Cold Chain Packaging Market, Middle East and Africa Cold Chain Packaging Market, and South and Central America Cold Chain Packaging Markets. These sections further fragment the regional Cold Chain Packaging market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways1. The report provides 2024 Cold Chain Packaging market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Cold Chain Packaging market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Cold Chain Packaging market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Cold Chain Packaging business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Cold Chain Packaging Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Cold Chain Packaging Pricing and Margins Across the Supply Chain, Cold Chain Packaging Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Cold Chain Packaging market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

Research Methodology

Our research methodology combines primary and secondary research techniques to ensure comprehensive market analysis.

Primary Research

We conduct extensive interviews with industry experts, key opinion leaders, and market participants to gather first-hand insights.

Secondary Research

Our team analyzes published reports, company websites, financial statements, and industry databases to validate our findings.

Data Analysis

We employ advanced analytical tools and statistical methods to process and interpret market data accurately.

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Global Cold Chain Packaging Market is estimated to generate USD 31 billion in revenue in 2024.

The Global Cold Chain Packaging Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 14.5% during the forecast period from 2025 to 2032.

The Cold Chain Packaging Market is estimated to reach USD 91.6 billion by 2032.

$3950- 30%

$6450- 40%

$8450- 50%

$2850- 20%

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!