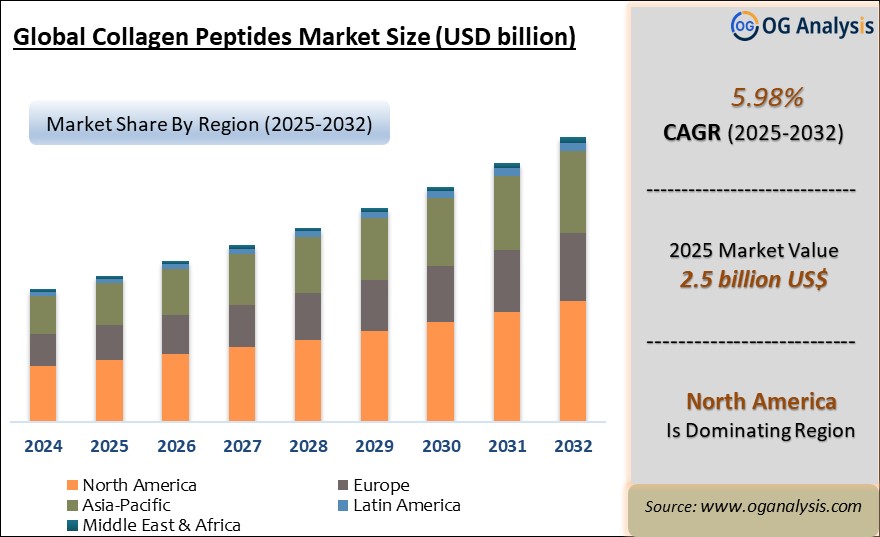

"The Global Collagen Peptides Market valued at USD 2.4 billion in 2024, is expected to grow by 5.98% CAGR to reach market size worth USD 4.4 billion by 2034."

The collagen peptides market, a rapidly evolving segment within the broader health and wellness industry, is experiencing phenomenal growth as consumers increasingly embrace the potential benefits of collagen for supporting joint health, skin elasticity, hair and nail strength, and overall wellbeing. Collagen peptides, derived from hydrolyzed collagen, are easily digestible protein fragments that are readily absorbed by the body, providing a convenient and effective way to boost collagen levels. The collagen peptides market is driven by the increasing popularity of collagen supplements, the growing awareness of the importance of collagen for maintaining health and vitality, and the growing demand for natural and effective solutions for supporting overall wellbeing.

In 2024, the collagen peptides market witnessed notable progress, with new and innovative collagen peptide products entering the market, the development of more bioavailable and effective formulations, and a growing emphasis on sustainability and ethical sourcing practices. These developments are expanding the reach of collagen peptides, making them more accessible and appealing to a wider range of consumers. The growth trajectory of the collagen peptides market is expected to continue in 2025, driven by the continued rise in consumer interest in collagen, the development of new and innovative applications, and the increasing integration of collagen peptides into a variety of food, beverage, and supplement products.

The Global Collagen Peptides Market Analysis Report will provide a comprehensive assessment of business dynamics, offering detailed insights into how companies can navigate the evolving landscape to maximize their market potential through 2034. This analysis will be crucial for stakeholders aiming to align with the latest industry trends and capitalize on emerging market opportunities.

North America is the leading region in the collagen peptides market, driven by rising consumer awareness of health and wellness, growing demand for functional foods and dietary supplements, and the increasing prevalence of joint and bone-related health issues.

Trade Intelligence for Collagen Peptides Market

| Global Peptones & protein substances Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 3,537 | 4,269 | 5,108 | 4,786 | 4,772 |

| United States of America | 545 | 729 | 905 | 848 | 763 |

| Netherlands | 433 | 479 | 532 | 549 | 516 |

| Germany | 276 | 326 | 451 | 424 | 430 |

| Japan | 296 | 337 | 376 | 356 | 319 |

| Canada | 146 | 181 | 216 | 188 | 210 |

| Source: OGAnalysis | |||||

- United States of America, Netherlands, Germany, Japan and Canada are the top five countries importing 46.9% of global Peptones & protein substances in 2024

- Global Peptones & protein substances Imports increased by 34.9% between 2020 and 2024

- United States of America accounts for 16% of global Peptones & protein substances trade in 2024

- Netherlands accounts for 10.8% of global Peptones & protein substances trade in 2024

- Germany accounts for 9% of global Peptones & protein substances trade in 2024

| Global Peptones & protein substances Export Prices, USD/Ton, 2020-24 |

| |

| Source: OGAnalysis |

Collagen Peptides Market Strategy, Price Trends, Drivers, Challenges and Opportunities to 2034

In terms of market strategy, price trends, drivers, challenges, and opportunities from2025 to 2034, Collagen Peptides market players are directing investments toward acquiring new technologies, securing raw materials through efficient procurement and inventory management, enhancing product portfolios, and leveraging capabilities to sustain growth amidst challenging conditions. Regional-specific strategies are being emphasized due to highly varying economic and social challenges across countries.

Factors such as global economic slowdown, the impact of geopolitical tensions, delayed growth in specific regions, and the risks of stagflation necessitate a vigilant and forward-looking approach among Collagen Peptides industry players. Adaptations in supply chain dynamics and the growing emphasis on cleaner and sustainable practices further drive strategic shifts within companies.

The market study delivers a comprehensive overview of current trends and developments in the Collagen Peptides industry, complemented by detailed descriptive and prescriptive analyses for insights into the market landscape until 2034.

North America Collagen Peptides Market Analysis

The North America Collagen Peptides market experienced notable developments in 2024, driven by rising consumer demand for premium, health-focused, and convenience-oriented products. Growth was further supported by innovations in product formulations and packaging, alongside increasing investments in advanced processing technologies. Anticipated growth from 2025 is underpinned by the region's robust distribution networks, a surge in plant-based alternatives, and growing awareness of sustainable production practices. The competitive landscape remains dynamic, with key players focusing on product diversification, strategic partnerships, and direct-to-consumer sales channels to capitalize on evolving consumer preferences. Regulatory advancements favoring clean-label and traceable sourcing also provide a strong growth foundation, positioning North America as a leading market for Collagen Peptides innovation.

Europe Collagen Peptides Market Outlook

In 2024, the Europe Collagen Peptides market demonstrated steady progress, buoyed by heightened interest in organic and eco-friendly offerings, alongside a growing preference for locally sourced ingredients. Anticipated growth from 2025 is supported by the increasing adoption of plant-based diets, government policies encouraging sustainable food systems, and advancements in manufacturing capabilities. The competitive landscape in Europe is marked by extensive R&D initiatives and collaborations between leading players and retailers to meet stringent quality standards and consumer expectations. Key market drivers include innovative packaging solutions, the popularity of premium segments, and rising e-commerce penetration, shaping a resilient and adaptive market environment.

Asia-Pacific Collagen Peptides Market Forecast

The Asia-Pacific Collagen Peptides market witnessed accelerated growth in 2024, spurred by urbanization, expanding middle-class demographics, and a shift toward convenient and functional foods. From 2025 onward, growth is expected to thrive on increasing disposable incomes, greater consumer awareness of health benefits, and the rapid expansion of online retail platforms. The competitive landscape is characterized by significant investments in regional production facilities and targeted marketing campaigns tailored to diverse consumer preferences. The adoption of advanced technologies, such as AI-driven personalization and blockchain-enabled supply chain transparency, is driving market differentiation and fostering trust among consumers.

Middle East, Africa, Latin America Collagen Peptides Market Overview

In 2024, the Middle East, Africa, Latin America Collagen Peptides market exhibited growth fueled by the increasing penetration of Western dietary trends, coupled with the growing influence of local cuisine innovations. Expected growth from 2025 is anchored in expanding infrastructure for food processing and distribution, as well as a rising focus on affordability and nutritional value. The competitive landscape highlights the strategic entry of global players through joint ventures and localized product offerings to cater to region-specific tastes and regulatory requirements. Sustainability initiatives and efforts to reduce food waste are becoming key differentiators, reinforcing the market's potential for long-term growth.

Collagen Peptides Market Dynamics and Future Analytics

The research analyses the Collagen Peptides parent market, derived market, intermediaries’ market, raw material market, and substitute market are all evaluated to better prospect the Collagen Peptides market outlook. Geopolitical analysis, demographic analysis, and Porter’s five forces analysis are prudently assessed to estimate the best Collagen Peptides market projections.

Recent deals and developments are considered for their potential impact on Collagen Peptides's future business. Other metrics analyzed include the Threat of New Entrants, Threat of New Substitutes, Product Differentiation, Degree of Competition, Number of Suppliers, Distribution Channel, Capital Needed, Entry Barriers, Govt. Regulations, Beneficial Alternative, and Cost of Substitute in Collagen Peptides market.

Collagen Peptides trade and price analysis helps comprehend Collagen Peptides's international market scenario with top exporters/suppliers and top importers/customer information. The data and analysis assist our clients in planning procurement, identifying potential vendors/clients to associate with, understanding Collagen Peptides price trends and patterns, and exploring new Collagen Peptides sales channels. The research will be updated to the latest month to include the impact of the latest developments such as the Russia-Ukraine war on the Collagen Peptides market.

Collagen Peptides Market Structure, Competitive Intelligence and Key Winning Strategies

The report presents detailed profiles of top companies operating in the Collagen Peptides market and players serving the Collagen Peptides value chain along with their strategies for the near, medium, and long term period.

OGAnalysis’ proprietary company revenue and product analysis model unveils the Collagen Peptides market structure and competitive landscape. Company profiles of key players with a business description, product portfolio, SWOT analysis, Financial Analysis, and key strategies are covered in the report. It identifies top-performing Collagen Peptides products in global and regional markets. New Product Launches, Investment & Funding updates, Mergers & Acquisitions, Collaboration & Partnership, Awards and Agreements, Expansion, and other developments give our clients the Collagen Peptides market update to stay ahead of the competition.

Company offerings in different segments across Asia-Pacific, Europe, the Middle East, Africa, and South and Central America are presented to better understand the company strategy for the Collagen Peptides market. The competition analysis enables users to assess competitor strategies and helps align their capabilities and resources for future growth prospects to improve their market share.

Collagen Peptides Market Research Scope

• Global Collagen Peptides market size and growth projections (CAGR), 2024- 2034

• Policies of USA New President Trump, Russia-Ukraine War, Israel-Palestine, Middle East Tensions Impact on the Collagen Peptides Trade and Supply-chain

• Collagen Peptides market size, share, and outlook across 5 regions and 27 countries, 2023- 2034

• Collagen Peptides market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2023- 2034

• Short and long-term Collagen Peptides market trends, drivers, restraints, and opportunities

• Porter’s Five Forces analysis, Technological developments in the Collagen Peptides market, Collagen Peptides supply chain analysis

• Collagen Peptides trade analysis, Collagen Peptides market price analysis, Collagen Peptides supply/demand

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products

• Latest Collagen Peptides market news and developments

The Collagen Peptides Market international scenario is well established in the report with separate chapters on North America Collagen Peptides Market, Europe Collagen Peptides Market, Asia-Pacific Collagen Peptides Market, Middle East and Africa Collagen Peptides Market, and South and Central America Collagen Peptides Markets. These sections further fragment the regional Collagen Peptides market by type, application, end-user, and country.

Report Scope

| Parameter | Collagen Peptides Market scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Source, By Form, By Application |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Regional Insights

North America Collagen Peptides market data and outlook to 2034

United States

Canada

Mexico

Europe Collagen Peptides market data and outlook to 2034

Germany

United Kingdom

France

Italy

Spain

BeNeLux

Russia

Asia-Pacific Collagen Peptides market data and outlook to 2034

China

Japan

India

South Korea

Australia

Indonesia

Malaysia

Vietnam

Middle East and Africa Collagen Peptides market data and outlook to 2034

Saudi Arabia

South Africa

Iran

UAE

Egypt

South and Central America Collagen Peptides market data and outlook to 2034

Brazil

Argentina

Chile

Peru

* We can include data and analysis of additional coutries on demand

Available Customizations

The standard syndicate report is designed to serve the common interests of Collagen Peptides Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below –

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Collagen Peptides Pricing and Margins Across the Supply Chain, Collagen Peptides Price Analysis / International Trade Data / Import-Export Analysis,

Supply Chain Analysis, Supply – Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Collagen Peptides market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days

Segmentation

By Source

- Bovine

- Porcine

- Marine & Poultry

By Form

- Dry

- Liquid

By Application

- Food & Beverages

- Nutritional Products

- Cosmetics & Personal Care Products

- Pharmaceuticals

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

-

Rousselot

-

GELITA AG

-

Resendable Group

-

Weishardt Holding SA

-

Juncà Gelatines SL

-

Xiamen Yiyu Biological Technology Co., Ltd.

-

Symatese

-

Collagen Matrix, Inc.

-

Collagen Solutions Plc

-

ConnOils LLC

-

Advanced BioMatrix, Inc.

-

Nitta Gelatin, NA Inc.

Recent Major Developments

- Freemen Nutra Group and RAWGA Inc. introduced the first clinically validated plant-based collagen peptide, derived from hibiscus, designed to stimulate collagen production more effectively than traditional animal-based options.

- Vital Proteins launched a ready-to-drink Collagen & Protein Shake with 30 g of protein and 10 g of collagen peptides, targeting the demand for convenient and functional wellness beverages.

- GELITA showcased its latest collagen peptide-based excipient innovations for pharmaceutical formulations, highlighting advancements in health and medical applications.

- ArcticCollagen expanded its sales channels by launching collagen peptide packets on Amazon, achieving around 20% growth in online distribution performance.

- HydroPeptide unveiled Collagen ReActivate PM, a nighttime lifting moisturizer with proprietary peptide technology and time-release retinol, aimed at significantly boosting collagen synthesis.

- Darling Ingredients and Tessenderlo Group announced a joint venture combining their collagen and gelatin businesses, creating a major global player with significant growth potential in nutrition and health sectors.

1. Table of Contents

1.1 List of Tables

1.2 List of Figures

2. Global Collagen Peptides Market Review, 2024

2.1 Collagen Peptides Industry Overview

2.2 Research Methodology

3. Collagen Peptides Market Insights

3.1 Collagen Peptides Market Trends to 2034

3.2 Future Opportunities in Collagen Peptides Market

3.3 Dominant Applications of Collagen Peptides, 2024 Vs 2034

3.4 Key Types of Collagen Peptides, 2024 Vs 2034

3.5 Leading End Uses of Collagen Peptides Market, 2024 Vs 2034

3.6 High Prospect Countries for Collagen Peptides Market, 2024 Vs 2034

4. Collagen Peptides Market Trends, Drivers, and Restraints

4.1 Latest Trends and Recent Developments in Collagen Peptides Market

4.2 Key Factors Driving the Collagen Peptides Market Growth

4.2 Major Challenges to the Collagen Peptides industry, 2025- 2034

4.3 Impact of Wars and geo-political tensions on Collagen Peptides supply chain

5 Five Forces Analysis for Global Collagen Peptides Market

5.1 Collagen Peptides Industry Attractiveness Index, 2024

5.2 Collagen Peptides Market Threat of New Entrants

5.3 Collagen Peptides Market Bargaining Power of Suppliers

5.4 Collagen Peptides Market Bargaining Power of Buyers

5.5 Collagen Peptides Market Intensity of Competitive Rivalry

5.6 Collagen Peptides Market Threat of Substitutes

6. Global Collagen Peptides Market Data – Industry Size, Share, and Outlook

6.1 Collagen Peptides Market Annual Sales Outlook, 2025- 2034 ($ Million)

6.1 Global Collagen Peptides Market Annual Sales Outlook by Type, 2025- 2034 ($ Million)

6.2 Global Collagen Peptides Market Annual Sales Outlook by Application, 2025- 2034 ($ Million)

6.3 Global Collagen Peptides Market Annual Sales Outlook by End-User, 2025- 2034 ($ Million)

6.4 Global Collagen Peptides Market Annual Sales Outlook by Region, 2025- 2034 ($ Million)

7. Asia Pacific Collagen Peptides Industry Statistics – Market Size, Share, Competition and Outlook

7.1 Asia Pacific Market Insights, 2024

7.2 Asia Pacific Collagen Peptides Market Revenue Forecast by Type, 2025- 2034 (USD Million)

7.3 Asia Pacific Collagen Peptides Market Revenue Forecast by Application, 2025- 2034(USD Million)

7.4 Asia Pacific Collagen Peptides Market Revenue Forecast by End-User, 2025- 2034 (USD Million)

7.5 Asia Pacific Collagen Peptides Market Revenue Forecast by Country, 2025- 2034 (USD Million)

7.5.1 China Collagen Peptides Analysis and Forecast to 2034

7.5.2 Japan Collagen Peptides Analysis and Forecast to 2034

7.5.3 India Collagen Peptides Analysis and Forecast to 2034

7.5.4 South Korea Collagen Peptides Analysis and Forecast to 2034

7.5.5 Australia Collagen Peptides Analysis and Forecast to 2034

7.5.6 Indonesia Collagen Peptides Analysis and Forecast to 2034

7.5.7 Malaysia Collagen Peptides Analysis and Forecast to 2034

7.5.8 Vietnam Collagen Peptides Analysis and Forecast to 2034

7.6 Leading Companies in Asia Pacific Collagen Peptides Industry

8. Europe Collagen Peptides Market Historical Trends, Outlook, and Business Prospects

8.1 Europe Key Findings, 2024

8.2 Europe Collagen Peptides Market Size and Percentage Breakdown by Type, 2025- 2034 (USD Million)

8.3 Europe Collagen Peptides Market Size and Percentage Breakdown by Application, 2025- 2034 (USD Million)

8.4 Europe Collagen Peptides Market Size and Percentage Breakdown by End-User, 2025- 2034 (USD Million)

8.5 Europe Collagen Peptides Market Size and Percentage Breakdown by Country, 2025- 2034 (USD Million)

8.5.1 2024 Germany Collagen Peptides Market Size and Outlook to 2034

8.5.2 2024 United Kingdom Collagen Peptides Market Size and Outlook to 2034

8.5.3 2024 France Collagen Peptides Market Size and Outlook to 2034

8.5.4 2024 Italy Collagen Peptides Market Size and Outlook to 2034

8.5.5 2024 Spain Collagen Peptides Market Size and Outlook to 2034

8.5.6 2024 BeNeLux Collagen Peptides Market Size and Outlook to 2034

8.5.7 2024 Russia Collagen Peptides Market Size and Outlook to 2034

8.6 Leading Companies in Europe Collagen Peptides Industry

9. North America Collagen Peptides Market Trends, Outlook, and Growth Prospects

9.1 North America Snapshot, 2024

9.2 North America Collagen Peptides Market Analysis and Outlook by Type, 2025- 2034($ Million)

9.3 North America Collagen Peptides Market Analysis and Outlook by Application, 2025- 2034($ Million)

9.4 North America Collagen Peptides Market Analysis and Outlook by End-User, 2025- 2034($ Million)

9.5 North America Collagen Peptides Market Analysis and Outlook by Country, 2025- 2034($ Million)

9.5.1 United States Collagen Peptides Market Analysis and Outlook

9.5.2 Canada Collagen Peptides Market Analysis and Outlook

9.5.3 Mexico Collagen Peptides Market Analysis and Outlook

9.6 Leading Companies in North America Collagen Peptides Business

10. Latin America Collagen Peptides Market Drivers, Challenges, and Growth Prospects

10.1 Latin America Snapshot, 2024

10.2 Latin America Collagen Peptides Market Future by Type, 2025- 2034($ Million)

10.3 Latin America Collagen Peptides Market Future by Application, 2025- 2034($ Million)

10.4 Latin America Collagen Peptides Market Future by End-User, 2025- 2034($ Million)

10.5 Latin America Collagen Peptides Market Future by Country, 2025- 2034($ Million)

10.5.1 Brazil Collagen Peptides Market Analysis and Outlook to 2034

10.5.2 Argentina Collagen Peptides Market Analysis and Outlook to 2034

10.5.3 Chile Collagen Peptides Market Analysis and Outlook to 2034

10.6 Leading Companies in Latin America Collagen Peptides Industry

11. Middle East Africa Collagen Peptides Market Outlook and Growth Prospects

11.1 Middle East Africa Overview, 2024

11.2 Middle East Africa Collagen Peptides Market Statistics by Type, 2025- 2034 (USD Million)

11.3 Middle East Africa Collagen Peptides Market Statistics by Application, 2025- 2034 (USD Million)

11.4 Middle East Africa Collagen Peptides Market Statistics by End-User, 2025- 2034 (USD Million)

11.5 Middle East Africa Collagen Peptides Market Statistics by Country, 2025- 2034 (USD Million)

11.5.1 South Africa Collagen Peptides Market Outlook

11.5.2 Egypt Collagen Peptides Market Outlook

11.5.3 Saudi Arabia Collagen Peptides Market Outlook

11.5.4 Iran Collagen Peptides Market Outlook

11.5.5 UAE Collagen Peptides Market Outlook

11.6 Leading Companies in Middle East Africa Collagen Peptides Business

12. Collagen Peptides Market Structure and Competitive Landscape

12.1 Key Companies in Collagen Peptides Business

12.2 Collagen Peptides Key Player Benchmarking

12.3 Collagen Peptides Product Portfolio

12.4 Financial Analysis

12.5 SWOT and Financial Analysis Review

14. Latest News, Deals, and Developments in Collagen Peptides Market

14.1 Collagen Peptides trade export, import value and price analysis

15 Appendix

15.1 Publisher Expertise

15.2 Collagen Peptides Industry Report Sources and Methodology

Research Methodology

Our research methodology combines primary and secondary research techniques to ensure comprehensive market analysis.

Primary Research

We conduct extensive interviews with industry experts, key opinion leaders, and market participants to gather first-hand insights.

Secondary Research

Our team analyzes published reports, company websites, financial statements, and industry databases to validate our findings.

Data Analysis

We employ advanced analytical tools and statistical methods to process and interpret market data accurately.

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Global Collagen Peptides Market is estimated to generate USD 2.5 billion in revenue in 2025

The Global Collagen Peptides Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.98% during the forecast period from 2025 to 2034.

The Collagen Peptides Market is estimated to reach USD 4.4 billion by 2034.

$3950- 30%

$5850- 40%

$7850- 50%

$2850- 20%

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!