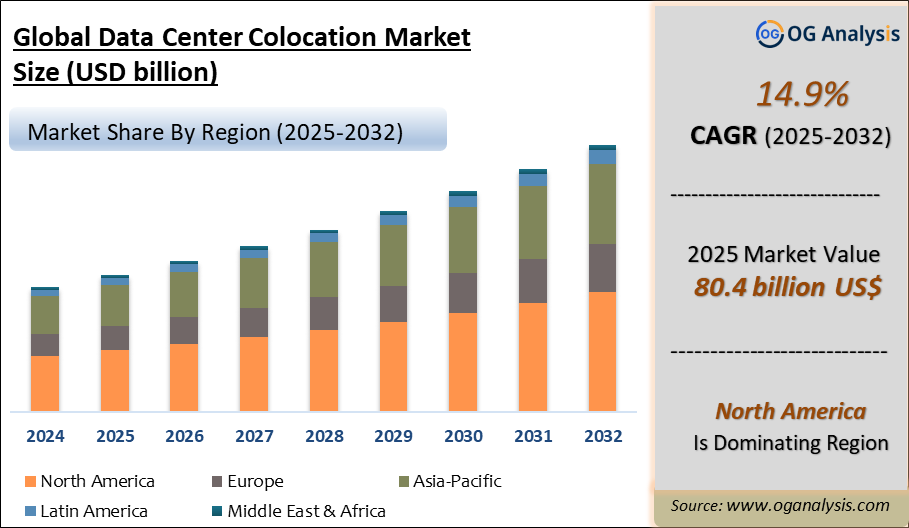

"The Global Data Center Colocation Market Size was valued at USD 71.3 billion in 2024 and is projected to reach USD 80.4 billion in 2025. Worldwide sales of Data Center Colocation are expected to grow at a significant CAGR of 14.9%, reaching USD 289.0 billion by the end of the forecast period in 2034."

Data Center Colocation Market Overview

The data center colocation market has experienced significant growth in recent years, driven by the increasing demand for scalable and cost-effective IT infrastructure solutions. Data center colocation refers to the practice of housing a company's IT equipment in a third-party data center facility, where space, power, cooling, and security are provided. This model allows businesses to leverage state-of-the-art infrastructure without the need for substantial capital investment in building and maintaining their own data centers. The market is witnessing robust expansion as enterprises across various industries seek to enhance their operational efficiency, scalability, and disaster recovery capabilities. The global data center colocation market was valued at approximately USD 50 billion in 2023 and is projected to reach USD 90 billion by 2030, growing at a CAGR of around 10% during the forecast period.

The growth of cloud computing, big data analytics, and IoT has significantly contributed to the demand for colocation services. Organizations are increasingly opting for colocation to manage their growing data storage and processing needs efficiently. Moreover, the shift towards remote work and digital transformation initiatives has further accelerated the adoption of colocation services. With the rising complexity of IT environments and the need for robust security and compliance measures, businesses are turning to colocation providers to ensure the reliability and security of their critical IT assets. This comprehensive market report delves into the various factors driving the growth of the data center colocation market, along with key trends, challenges, and major players in the industry.

Global Data Center Colocation Market Analysis 2025-2032: Industry Size, Share, Growth Trends, Competition and Forecast Report

Data Center Colocation Market- Latest Trends, Drivers, Challenges

One of the most significant trends in the data center colocation market is the increasing adoption of hybrid IT environments. Organizations are leveraging a combination of on-premise, cloud, and colocation services to optimize their IT infrastructure and achieve greater flexibility and scalability. This trend is driven by the need to balance workloads across different environments while maintaining control over critical data and applications. Another notable trend is the growing emphasis on sustainability and energy efficiency. Data center operators are investing in green technologies and renewable energy sources to reduce their carbon footprint and meet regulatory requirements. The use of advanced cooling techniques, energy-efficient hardware, and AI-driven energy management systems is becoming more prevalent in colocation facilities.

The rise of edge computing is also shaping the data center colocation market. With the proliferation of IoT devices and the need for real-time data processing, businesses are increasingly deploying edge data centers closer to the data source. Colocation providers are expanding their services to include edge facilities, offering low-latency connectivity and enhanced performance for latency-sensitive applications. Additionally, the integration of artificial intelligence and machine learning in data center operations is gaining traction. AI-powered tools are being used for predictive maintenance, capacity planning, and optimizing resource utilization, resulting in improved operational efficiency and reduced downtime.

Several key drivers are propelling the growth of the data center colocation market. The rapid digital transformation across industries is a primary driver, as businesses seek reliable and scalable IT infrastructure to support their digital initiatives. The increasing adoption of cloud services is also a significant factor, as colocation provides the necessary connectivity and infrastructure to support hybrid cloud deployments. Cost efficiency is another crucial driver, as colocation allows organizations to reduce their capital expenditures and operational costs associated with building and maintaining data centers. Moreover, the growing need for robust disaster recovery and business continuity solutions is driving the demand for colocation services, as they offer geographically dispersed facilities with high availability and redundancy.

Despite the positive growth outlook, the data center colocation market faces several challenges. One of the primary challenges is the high initial setup cost for colocation services, which can be a barrier for small and medium-sized enterprises (SMEs). Ensuring data security and compliance with regulatory standards is another significant challenge, as colocation providers must implement stringent security measures to protect sensitive customer data. Additionally, the rapidly evolving technology landscape requires continuous investment in infrastructure upgrades and innovation to stay competitive. The increasing demand for energy-efficient operations and sustainable practices also poses a challenge, as data center operators must balance energy consumption with performance and cost-effectiveness. Addressing these challenges requires strategic planning, investment in advanced technologies, and a focus on delivering exceptional service quality to meet customer expectations.

Major Players in the Data Center Colocation Market

1. Equinix, Inc.

2. Digital Realty Trust, Inc.

3. CyrusOne Inc.

4. Global Switch

5. China Telecom Corporation Limited

6. NTT Communications Corporation

7. KDDI Corporation

8. Interxion Holding N.V.

9. Telehouse

10. Cyxtera Technologies, Inc.

11. QTS Realty Trust, Inc.

12. CoreSite Realty Corporation

13. Iron Mountain Incorporated

14. ST Telemedia Global Data Centres (STT GDC)

15. Flexential Corp.

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product, By Enterprise, and By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type:

Retail Colocation

Wholesale Colocation

By Enterprise Size:

Small and Medium Enterprises (SMEs)

Large Enterprises

By End User:

BFSI

IT and Telecommunications

Healthcare

Government and Public Sector

Retail

Energy

Others

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Data Center Colocation Market is estimated to reach USD 216.6 billion by 2032.

The Global Data Center Colocation Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 14.9% during the forecast period from 2025 to 2032.

The Global Data Center Colocation Market is estimated to generate USD 71.3 billion in revenue in 2024.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!