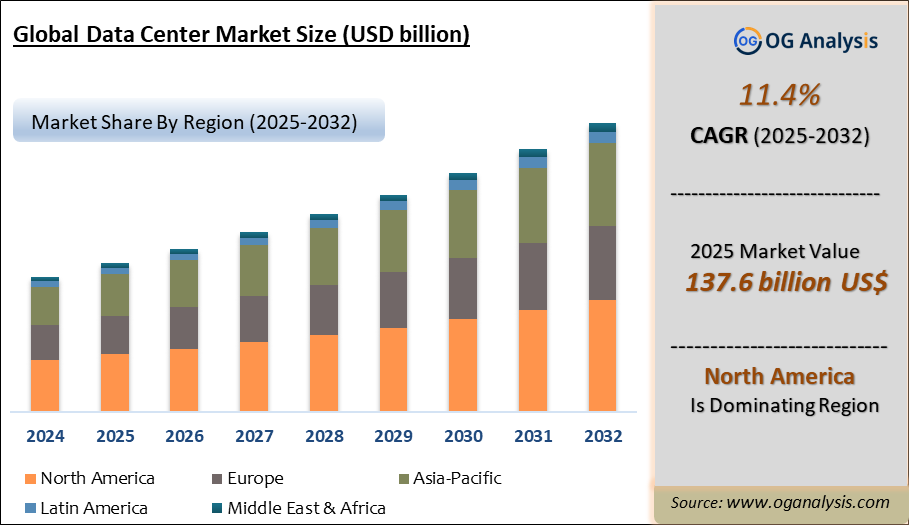

"The Global Data Center Market Size was valued at USD 125.4 billion in 2024 and is projected to reach USD 137.6 billion in 2025. Worldwide sales of Data Center are expected to grow at a significant CAGR of 11.4%, reaching USD 372.7 billion by the end of the forecast period in 2034."

The global data center market witnessed strong growth in 2023 driven by rapid digital transformation, rising cloud adoption, and surging AI workloads requiring advanced computing infrastructure. Data centers include physical facilities housing servers, storage, networking equipment, and supporting infrastructure such as power and cooling systems to ensure continuous and efficient data processing and storage. Growing demand for hyperscale, colocation, and edge data centers is supported by increasing internet penetration, smart technologies, and enterprise IT expansion. North America leads in market share with established operators, while Asia-Pacific is witnessing the fastest growth due to rising digital economies, cloud investments, and emerging data sovereignty regulations. Key players focus on capacity expansions, sustainable data center designs, and strategic partnerships to strengthen market positioning globally.

The market is also seeing a shift towards green data centers with renewable energy integration, efficient cooling, and low PUE architectures to meet corporate sustainability goals. However, challenges such as rising power demands, land scarcity in urban hubs, and high capital investments remain critical constraints. Technological advancements in modular data centers, AI-integrated facility management, and software-defined data center architectures are transforming deployment models, enhancing scalability, efficiency, and operational resilience. Overall, the market is expected to maintain robust growth as digitalisation, AI, IoT, and 5G technologies drive demand for reliable, secure, and energy-efficient data center infrastructure worldwide.

By type, cloud data centers are the fastest-growing segment driven by the rapid adoption of cloud computing, AI workloads, and digital transformation initiatives across industries. Enterprises are shifting from traditional infrastructure to scalable, flexible, and cost-efficient cloud data centers to support dynamic business operations and storage requirements globally.

By end user, IT & telecommunications is the largest segment as data centers are critical for hosting, processing, and managing massive volumes of data generated by digital services, internet usage, and telecom networks. The sector continues to drive demand with investments in 5G, IoT, and AI, requiring robust and scalable data center infrastructure worldwide.

Key Insights

- The market is driven by surging cloud computing demand as enterprises increasingly migrate workloads to public and hybrid clouds, creating strong need for scalable, secure, and low-latency data center infrastructure globally to support seamless digital transformation.

- North America remains the largest market due to established hyperscale and colocation operators, high internet penetration, and AI investments, while Asia-Pacific is witnessing fastest growth driven by expanding cloud services, digitalisation initiatives, and rising data sovereignty regulations in key economies.

- Hyperscale data centers are a dominant segment supported by major cloud service providers expanding global footprints to accommodate AI training, large data storage, and high-performance computing workloads across industries.

- Green data center initiatives are gaining momentum as operators integrate renewable power, advanced cooling technologies, and low-carbon designs to achieve sustainability targets and reduce operational costs amid rising environmental concerns.

- Edge data centers are witnessing growing demand to support 5G networks, IoT deployments, and latency-sensitive applications by bringing compute and storage resources closer to end users, enhancing network efficiency and user experience.

- High energy consumption remains a critical challenge with data centers accounting for significant global electricity use, prompting companies to invest in energy-efficient technologies, AI-enabled cooling optimisation, and renewable energy sourcing for operational sustainability.

- Technological advancements in software-defined data centers (SDDC) are enabling greater agility, automation, and scalability, allowing operators to manage diverse workloads efficiently while optimising resource utilisation and reducing operational complexities.

- Major companies are investing in modular and prefabricated data center solutions to reduce construction timelines, lower capital costs, and enable rapid deployment for meeting dynamic workload demands in both developed and emerging markets.

- Rising AI and machine learning workloads are creating demand for GPU-rich, high-density data centers capable of supporting training models, real-time analytics, and inferencing applications with robust power and cooling infrastructure.

- Partnerships between data center operators, cloud providers, and technology companies are strengthening to co-develop advanced facilities, integrate edge and core infrastructure, and expand regional capacities to meet growing digital economy needs efficiently.

Reort Scope

| Parameter | Detail |

|---|---|

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By End User |

| Countries Covered | North America (USA, Canada, Mexico) Europe (Germany, UK, France, Spain, Italy, Rest of Europe) Asia-Pacific (China, India, Japan, Australia, Rest of APAC) The Middle East and Africa (Middle East, Africa) South and Central America (Brazil, Argentina, Rest of SCA) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10 % free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Datafile |

Market Segmentation

- By Type:

- Enterprise Data Centers

- Managed Services Data Centers

- Colocation Data Centers

- Cloud Data Centers

- By End User:

- IT & Telecommunications

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- Government

- Energy

- Retail

- Manufacturing

- By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

What You Receive

• Global Data Center market size and growth projections (CAGR), 2024- 2034• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Data Center.

• Data Center market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Data Center market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Data Center market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Data Center market, Data Center supply chain analysis.

• Data Center trade analysis, Data Center market price analysis, Data Center Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Data Center market news and developments.

The Data Center Market international scenario is well established in the report with separate chapters on North America Data Center Market, Europe Data Center Market, Asia-Pacific Data Center Market, Middle East and Africa Data Center Market, and South and Central America Data Center Markets. These sections further fragment the regional Data Center market by type, application, end-user, and country.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways1. The report provides 2024 Data Center market sales data at the global, regional, and key country levels with a detailed outlook to 2034, allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Data Center market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Data Center market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Data Center business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Data Center Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below :

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Data Center Pricing and Margins Across the Supply Chain, Data Center Price Analysis / International Trade Data / Import-Export Analysis

Supply Chain Analysis, Supply–Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Data Center market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days.

Research Methodology

Our research methodology combines primary and secondary research techniques to ensure comprehensive market analysis.

Primary Research

We conduct extensive interviews with industry experts, key opinion leaders, and market participants to gather first-hand insights.

Secondary Research

Our team analyzes published reports, company websites, financial statements, and industry databases to validate our findings.

Data Analysis

We employ advanced analytical tools and statistical methods to process and interpret market data accurately.

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Global Data Center Market is estimated to generate USD 125.4 billion in revenue in 2024.

The Global Data Center Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 11.4% during the forecast period from 2025 to 2032.

The Data Center Market is estimated to reach USD 297.4 billion by 2032.

$4150- 30%

$6450- 40%

$8450- 50%

$2850- 20%

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!