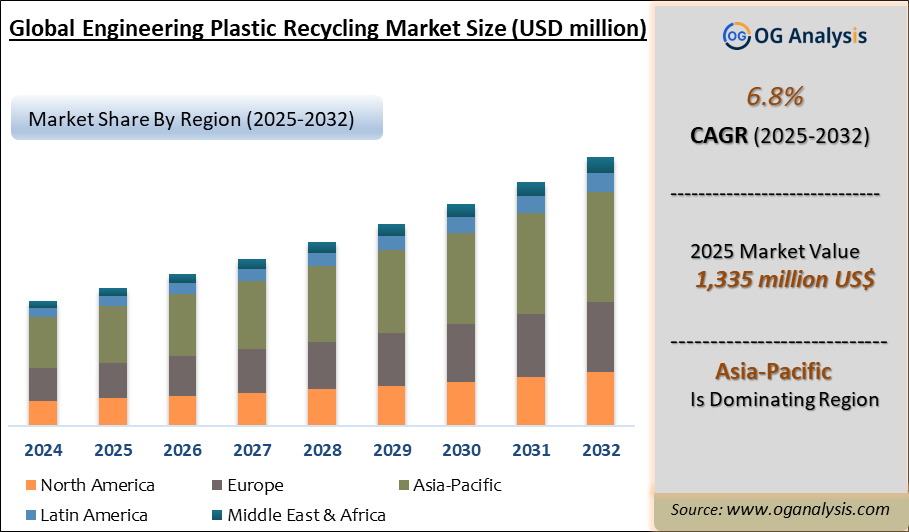

"The Engineering Plastic Recycling Market Size was valued at USD 1,426 million in 2026. Worldwide sales of Engineering Plastic Recycling are expected to grow at a significant CAGR of 6.8%, reaching $ 2,462 million by the end of the forecast period in 2034."

The Engineering Plastic Recycling Market is gaining importance as industries shift from linear plastic consumption toward circular material systems. Engineering plastics such as polycarbonate, polyamide, ABS, PBT, PET, and high-performance blends are widely used in automotive, electrical and electronics, industrial components, packaging, consumer goods, and machinery due to their durability, heat resistance, dimensional stability, and mechanical strength. Recycling these plastics helps reduce landfill burden, lower dependence on virgin polymers, and support sustainability commitments across manufacturing supply chains. Regulatory pressure is also strengthening, with the EU’s Packaging and Packaging Waste Regulation entering into force in February 2025 and requiring all packaging placed on the EU market to be recyclable in an economically viable way by 2030.

Market growth is being supported by rising demand for recycled engineering-grade resins from automotive, electronics, packaging, and industrial users. Mechanical recycling remains widely used, while chemical recycling, depolymerization, solvent-based recycling, and advanced sorting technologies are improving the quality and consistency of recycled materials. Automotive recycling rules are also evolving, with the EU Council agreeing in June 2025 on requirements for vehicles to be designed for reuse and recycling, including targets for recycled plastics in vehicle production. However, the market continues to face challenges such as contamination, inconsistent waste streams, high processing costs, quality degradation, limited traceability, and competition from low-cost virgin plastics.

Regional Analysis

North America Engineering Plastic Recycling Market

North America is a major market for engineering plastic recycling, supported by strong automotive, electrical and electronics, packaging, appliances, and industrial manufacturing sectors. The United States leads regional demand as OEMs and brand owners increase the use of recycled polycarbonate, ABS, polyamide, PET, PBT, and other high-performance recycled polymers to meet sustainability targets. The region is also seeing growing interest in chemical recycling, advanced sorting, compounding, and recycled-content certification. However, inconsistent collection systems, contamination, quality variation, and cost competitiveness against virgin resins remain key challenges.

Europe Engineering Plastic Recycling Market

Europe is one of the most regulation-driven markets for engineering plastic recycling, supported by circular economy policies, recycled-content targets, end-of-life vehicle initiatives, and strict waste management standards. Germany, France, Italy, the UK, Spain, and the Nordic countries are key demand centers due to strong automotive, electronics, industrial machinery, and packaging industries. The EU’s focus on plastics circularity is encouraging higher recycling rates, improved design-for-recycling, and greater use of recycled plastics in vehicles and durable goods. Recycled engineering plastics are gaining traction in automotive interiors, electrical housings, appliance parts, and technical components.

Asia-Pacific Engineering Plastic Recycling Market

Asia-Pacific holds a leading position in the engineering plastic recycling market due to its large plastic processing base, strong electronics manufacturing, rapid automotive production, and growing industrial demand. China, India, Japan, South Korea, and Southeast Asia are key contributors, with strong recycling opportunities in ABS, polycarbonate, PET, polyamide, and PC-ABS blends. The region benefits from high volumes of post-industrial and post-consumer plastic waste, especially from electronics, appliances, automotive parts, and packaging. Asia-Pacific accounted for the largest revenue share in recycled engineering plastics in 2024, supported by expanding automotive and electronics industries.

Middle East & Africa Engineering Plastic Recycling Market

The Middle East & Africa market is gradually developing, supported by rising plastic waste management initiatives, industrial diversification, construction growth, packaging demand, and expanding automotive aftermarket activity. Gulf countries are investing in recycling infrastructure and circular economy programs as part of broader sustainability and localization strategies. South Africa remains one of the more established recycling markets in the region, supported by packaging, automotive components, electrical goods, and industrial plastic waste recovery. However, the region still faces challenges such as limited high-grade sorting infrastructure, informal collection systems, lower recycled engineering plastic quality consistency, and dependence on imported technology.

South & Central America Engineering Plastic Recycling Market

South & Central America offers growing opportunities for engineering plastic recycling, led by Brazil, Mexico, Argentina, Chile, and Colombia. Brazil and Mexico are important demand centers due to their automotive, electronics, packaging, appliance, and industrial manufacturing bases. Recycled polycarbonate, ABS, PET, PP compounds, and other technical plastics are gaining relevance in automotive components, consumer goods, electrical housings, and durable products. The region also benefits from strong informal and semi-formal recycling networks, though limited advanced sorting, inconsistent waste collection, and quality standardization remain barriers. Growth is expected to improve as manufacturers increase recycled-content use and local recycling infrastructure matures.

Trade Intelligence for engineering plastic recycling market

| Global parings and scrap of plastics (excl. that of polymers of ethylene Trade, Imports, USD million, 2020-24 | |||||

|

| 2020 | 2021 | 2022 | 2023 | 2024 |

| World | 1,284 | 1,749 | 2,161 | 1,578 | 1,659 |

| United States of America | 184 | 270 | 292 | 246 | 314 |

| Taipei, Chinese | 96 | 131 | 159 | 121 | 142 |

| Netherlands | 88 | 175 | 269 | 175 | 129 |

| Türkiye | 64 | 70 | 116 | 79 | 84 |

| Viet Nam | 98 | 138 | 126 | 87 | 75 |

| Source: OGAnalysis, International Trade Centre (ITC) | |||||

- United States of America, Taipei, Chinese, Netherlands, Türkiye and Viet Nam are the top five countries importing 44.8% of global parings and scrap of plastics (excl. that of polymers of ethylene in 2024

- Global parings and scrap of plastics (excl. that of polymers of ethylene Imports increased by 29.2% between 2020 and 2024

- United States of America accounts for 18.9% of global parings and scrap of plastics (excl. that of polymers of ethylene trade in 2024

- Taipei, Chinese accounts for 8.6% of global parings and scrap of plastics (excl. that of polymers of ethylene trade in 2024

- Netherlands accounts for 7.8% of global parings and scrap of plastics (excl. that of polymers of ethylene trade in 2024

| Global parings and scrap of plastics (excl. that of polymers of ethylene Export Prices, USD/Ton, 2020-24 |

|

|

| Source: OGAnalysis |

Key Insights

- Engineering plastic recycling demand is supported by rising sustainability goals and circular economy commitments across automotive, electronics, packaging, and industrial sectors. Companies are increasingly using recycled polymers to reduce carbon footprint, improve resource efficiency, and meet customer-driven environmental targets.

- Polycarbonate, ABS, polyamide, PET, PBT, and POM remain key recycled engineering plastic categories due to their strong use in high-performance applications. These materials offer durability, heat resistance, dimensional stability, and mechanical strength required in automotive parts, electronics housings, appliances, and industrial components.

- Automotive applications are creating strong opportunities for recycled engineering plastics in interior, exterior, underbody, and technical components. Automakers are using recycled plastics to support vehicle lightweighting, lower emissions, cost optimization, and compliance with sustainability-focused procurement standards.

- Electrical and electronics waste is becoming an important feedstock source for engineering plastic recycling. Recycled ABS, PC, and PC-ABS blends are increasingly used in device housings, keyboards, appliances, display panels, connectors, and other durable electronic components.

- Mechanical recycling remains the leading recycling process due to lower processing cost, established infrastructure, and suitability for clean post-industrial waste streams. However, recycled output quality depends heavily on sorting accuracy, contamination removal, polymer purity, and additive compatibility.

- Chemical recycling and solvent-based recycling are gaining attention for difficult-to-recycle engineering plastics and mixed waste streams. These technologies can improve material recovery from contaminated, multilayer, flame-retardant, and high-specification polymer waste where conventional mechanical recycling is limited.

- Regulatory pressure is strengthening market development, especially in Europe and North America. Policies supporting recycled-content use, waste traceability, circular product design, and plastic waste reduction are encouraging manufacturers to invest in higher-quality recycling systems.

- Quality consistency remains one of the most important market challenges for recycled engineering plastics. Automotive, electronics, and industrial buyers require predictable mechanical performance, color stability, flame resistance, thermal properties, and long-term durability before approving recycled grades.

- Advanced sorting, AI-based identification, washing, compounding, and additive technologies are improving recycled engineering plastic quality. These solutions help recyclers separate complex polymer streams, upgrade material properties, and produce application-specific recycled compounds.

- Asia-Pacific is expected to remain a major growth region due to large automotive, electronics, appliance, and plastic processing industries. Europe is advancing through regulation-led circularity, while North America benefits from OEM sustainability programs and growing demand for high-performance recycled polymers.

Report Scope

| Parameter | Engineering Plastic Recycling Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type and By End-User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Type

- Polycarbonate (PC)

- Polyethylene Terephthalate (PET)

- Styrene Copolymers (ABS and SAN)

- Polyamide (PA)

- Polybutylene Terephthalate (PBT)

- Other Engineering Plastics

By End-user Industry

- Packaging

- Industrial Yarn

- Electrical and Electronics

- Building and Construction

- Automotive

- Other End-user Industries

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- EF Plastics UK Limited

- Euresi Plastics SL

- Kuusakoski

- MBA Polymers Inc.

- Mumford Industries

- Pistoni Srl

- PolyClean Technologies

- Teijin Limited

- Alpek Polyester

- Centriforce Products Limited

- Clean Tech UK Ltd

- Far Eastern New Century Corporation

- Foss Performance Materials

- Indorama Ventures Public Company Limited

- JFC Group

- Lotte Chemical Corporation

- PETCO

- Placon

- PolyQuest

- Reliance Industries Limited

- REPRO-PET

- UltrePET LLC

- Verdeco Recycling Inc.

Recent Developments

May 2026: Polykemi and Rondo Plast expanded recycled-material capacity in Sweden, adding a ReadyMac unit after an earlier Erema investment. The expansion enables processing of PCR-based engineering plastics such as PC, ABS, PS, and PA, strengthening supply for high-quality recycled compounds.

December 2025: Toyota Tsusho announced that ASR-derived recycled plastic produced by its group company Planic was adopted in the underbody cover of Toyota’s new RAV4. This marked an important step in using automotive shredder residue as a source for vehicle-grade recycled plastic components.

December 2025: Samsara Eco advanced enzymatic recycling technology targeting difficult-to-recycle automotive plastics, including nylon 66, nylon 6, polyester, and mixed plastic-fiber streams. The development supports circularity for EV and automotive components that require heat-resistant engineering polymers.

October 2025: BASF presented two recycling processes for polyamide 6 from end-of-life vehicles, including depolymerization and solvent-based recycling. Pilot projects with ZF and Pöppelmann demonstrated near-series applications for Mercedes-Benz components.

October 2025: BASF and ETH Zurich highlighted gasification of automotive shredder residue with biomass as a route to produce non-fossil feedstock. The study showed potential to reduce emissions and recover value from mixed plastic waste streams that are difficult to recycle mechanically.

September 2025: BASF, Porsche, and BEST completed a pilot project on chemical recycling of mixed end-of-life vehicle waste. The project demonstrated that complex residues such as plastics, films, paints, and foams can be converted into raw materials for new vehicle components.

June–December 2025: EU institutions advanced new end-of-life vehicle circularity rules, including phased recycled-plastic targets for new vehicles. The agreement supports long-term demand for recycled automotive plastics and closed-loop plastic recovery from end-of-life vehicles.

May 2025: Toyoda Gosei launched horizontal recycling technology for plastic automotive parts using end-of-life vehicle plastics. The company developed recycled polypropylene containing 50% ELV plastic with performance suitable for automotive interior parts, starting with Toyota Camry applications.

FAQ's

The Global Engineering Plastic Recycling Market is estimated to generate USD 1,426 million in revenue in 2026.

The Global Engineering Plastic Recycling Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% during the forecast period from 2026 to 2032.

The Engineering Plastic Recycling Market is estimated to reach USD 2134.4 million by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!