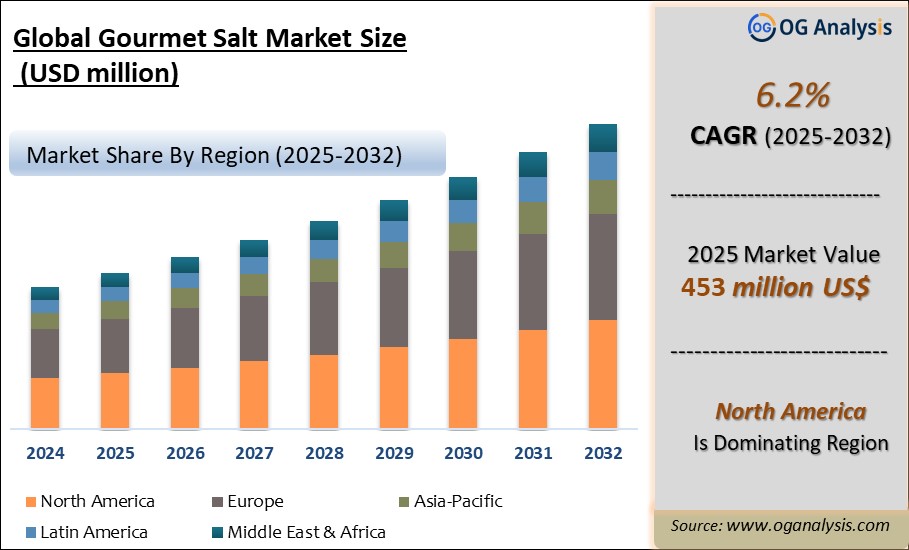

"The Gourmet Salt Market Size was valued at $ 481 million in 2026. Worldwide sales of Gourmet Salt are expected to grow at a significant CAGR of 6.2%, reaching $ 791 million by the end of the forecast period in 2034."

The Gourmet Salt Market is a specialized segment of premium seasoning ingredients, specialty food products, culinary finishing salts, natural mineral salts, artisanal sea salts, flavored salts, and value-added foodservice ingredients, serving household consumers, restaurants, hotels, gourmet food brands, seasoning manufacturers, snack producers, bakery companies, meat processors, confectionery brands, and premium retail channels. Gourmet salt includes sea salt, Himalayan pink salt, fleur de sel, sel gris, smoked salt, black salt, flake salt, kosher-style coarse salt, infused salt, truffle salt, herb salt, chili salt, and mineral-rich specialty salts. These products are valued for texture, crystal size, color, origin, flavor intensity, finishing appeal, and culinary differentiation rather than basic sodium functionality. Sea salt is produced through seawater evaporation, while rock and mineral salts are mined from underground deposits, with product appeal often linked to origin, appearance, processing method, and chef-led usage.

The market is gaining traction as consumers increasingly seek premium cooking experiences, restaurant-style plating, clean-label seasonings, artisanal food products, and differentiated flavor profiles. Gourmet salts are used in grilled meats, seafood, salads, chocolate, caramel, bakery products, snacks, sauces, spice blends, cocktails, vegan foods, and premium packaged foods. Key trends include natural sea salts, smoked salts, flavored salts, coarse finishing salts, traceable origin salts, chef-inspired seasoning blends, gift packaging, organic-positioned products, and premium salts for home cooking and foodservice. Growth is supported by gourmet retail, online specialty food sales, culinary tourism, social media cooking content, premium snacking, and demand for visually appealing food ingredients. However, challenges include sodium-reduction awareness, consumer confusion around health claims, price sensitivity, supply consistency, food safety requirements, and competition from spice blends, low-sodium seasonings, herbs, and umami ingredients. Public health agencies continue to recommend limiting sodium intake, which creates pressure on all salt categories, including premium and gourmet salts.

Regional Analysis

North America Gourmet Salt Market

North America Gourmet Salt Market is supported by strong demand from premium home cooking, specialty food retail, restaurants, gourmet seasoning brands, snack manufacturers, and e-commerce food platforms. The United States remains the leading regional market, driven by consumer interest in restaurant-style cooking, flavored salts, smoked salts, finishing salts, Himalayan pink salt, sea salt flakes, and premium spice blends. Specialty food demand continues to support premium ingredients, with industry trends highlighting upscaled home cooking and premium food experiences as important growth themes. However, sodium-reduction initiatives remain an important restraint, especially for packaged food manufacturers and foodservice operators that must balance flavor enhancement with public health guidance. FDA sodium-reduction efforts continue to focus on commercially processed, packaged, and prepared foods, which influences how gourmet salts are positioned in food applications.

Asia Pacific Gourmet Salt Market

Asia Pacific Gourmet Salt Market is one of the most diverse regional markets, supported by traditional salt production, premium food culture, rising middle-class consumption, expanding modern retail, and strong use of specialty salts in both cooking and wellness-positioned products. China, India, Japan, South Korea, Australia, Indonesia, Thailand, and Vietnam are key contributors. Demand is rising for sea salt, Himalayan pink salt, black salt, rock salt, bamboo salt, smoked salt, flavored salt, and premium finishing salts used in home cooking, restaurants, packaged foods, snacks, pickles, seasonings, and gifting products. Japan and South Korea support demand for refined culinary salts and specialty seasonings, while India has strong interest in rock salt, black salt, and Himalayan-origin salts. However, the region also faces increasing sodium-awareness campaigns, and public health discussions around salt intake may influence long-term product positioning. Suppliers are expected to benefit from origin storytelling, premium packaging, foodservice adoption, and clean-label seasoning trends.

Europe Gourmet Salt Market

Europe Gourmet Salt Market is shaped by strong culinary traditions, premium food culture, artisanal sourcing, luxury retail, organic food demand, and sustainability-led consumer preferences. France, Italy, Spain, Germany, the United Kingdom, the Netherlands, Greece, Portugal, and Nordic countries are important markets due to high usage of sea salt, fleur de sel, sel gris, flake salt, smoked salt, herb-infused salt, and gourmet finishing salts in restaurants, bakeries, meat products, cheese, seafood, confectionery, and premium packaged foods. Europe has a strong base of artisanal salt producers and origin-linked products, particularly in coastal salt-producing regions. At the same time, sodium-reduction policies and health-focused food reformulation continue to influence the category. The European Commission notes that voluntary national salt initiatives have been part of broader efforts to reduce salt content across foods and catering, which encourages careful positioning of gourmet salts as culinary enhancers rather than health products.

Middle East & Africa Gourmet Salt Market

Middle East & Africa Gourmet Salt Market is developing through demand from hotels, restaurants, premium retail, gourmet food stores, meat processing, spice blends, bakery products, and luxury hospitality channels. Gulf countries are important demand centers due to premium foodservice, international cuisine, tourism, modern grocery retail, and demand for imported gourmet ingredients. Products such as Himalayan pink salt, sea salt flakes, smoked salt, black salt, flavored salt, and gift-packaged seasoning blends are gaining visibility among higher-income consumers and hospitality buyers. South Africa also contributes through modern retail, foodservice, artisanal food brands, and premium seasoning demand. Africa’s wider market remains more price-sensitive, with gourmet salt adoption concentrated in urban, premium, and imported-food channels. Opportunities exist in chef-led usage, halal-positioned seasoning blends, gourmet gifting, premium meat and barbecue applications, and tourism-linked foodservice. However, import dependence, price sensitivity, limited consumer awareness, and competition from conventional salt and spice blends remain key challenges.

South & Central America Gourmet Salt Market

South & Central America Gourmet Salt Market is supported by culinary diversity, barbecue culture, restaurant growth, premium retail, food gifting, snack seasoning, and expanding interest in artisanal ingredients. Brazil, Mexico, Argentina, Chile, Colombia, Peru, and Costa Rica are important markets due to strong food culture, meat consumption, hospitality demand, and growing use of premium seasonings in home cooking and foodservice. Demand is rising for coarse sea salt, smoked salt, flavored salt, chili salt, herb salt, finishing salts, and gourmet blends used in grilled meats, seafood, snacks, sauces, confectionery, and packaged foods. Mexico and Brazil offer strong opportunities in flavored and spice-infused salts, while Argentina and Chile support demand through grilling, premium meats, seafood, and wine-pairing cuisine. However, economic volatility, import costs, affordability constraints, and sodium-reduction awareness can limit premium adoption. Future growth will depend on local artisanal brands, foodservice education, attractive packaging, e-commerce specialty foods, and positioning gourmet salt as a flavor-finishing ingredient used in controlled quantities.

Key Insights

- Premium home cooking is one of the strongest growth drivers for the Gourmet Salt Market. Consumers increasingly use specialty salts to enhance everyday meals, replicate restaurant-style presentation, and add finishing texture to dishes. Flake salts, sea salts, smoked salts, and infused salts are gaining popularity among home cooks who seek simple ways to upgrade flavor and appearance.

- Foodservice and chef-led demand strongly influence market development. Restaurants, hotels, bakeries, premium cafés, steakhouses, seafood restaurants, and gourmet kitchens use specialty salts for finishing, curing, grilling, baking, and plating. Chef endorsement helps educate consumers about salt texture, origin, crystal shape, and application-specific use, supporting wider retail adoption.

- Sea salt remains a major product category due to its natural positioning, broad culinary use, and availability in fine, coarse, flake, and finishing formats. It is widely used in cooking, seasoning blends, bakery toppings, seafood dishes, snacks, and gourmet packaged foods. Its appeal is linked to simplicity, texture, and perceived artisanal value.

- Himalayan pink salt continues to attract consumers because of its distinctive pink color, mineral-origin story, and strong shelf appeal. It is used in grinders, slabs, seasoning blends, bath products, foodservice presentation, and premium retail packs. However, its value proposition is driven more by visual appeal and origin-based marketing than by meaningful sodium-reduction benefits.

- Fleur de sel and flake salts are important premium finishing salts. They are typically used at the end of cooking to add delicate crunch, surface flavor, and visual refinement to meats, vegetables, chocolates, desserts, salads, and bakery products. Their higher price positioning makes them attractive for gourmet retailers, chefs, and premium food brands.

- Flavored and infused salts are expanding product innovation. Truffle salt, smoked salt, garlic salt, chili salt, herb salt, lemon salt, wine salt, and charcoal salt allow brands to combine seasoning convenience with premium positioning. These products are especially relevant in snacks, grilling, cocktails, gifting, ready-to-cook foods, and specialty spice blends.

- Packaging and branding are key competitive factors. Gourmet salt is often sold in glass jars, grinders, tins, pouches, gift boxes, refill packs, and chef-inspired collections. Origin storytelling, premium labels, transparent sourcing, attractive colors, and application guidance help brands differentiate in retail, e-commerce, and gifting channels.

- Health and sodium concerns remain important restraints. Gourmet salts may differ in texture, taste, and appearance, but they are still primarily sodium chloride. Consumers, retailers, and food manufacturers are increasingly aware of sodium intake guidelines, which creates pressure for portion control, responsible labeling, and balanced product positioning.

- Clean-label and natural food trends support demand, but claims require care. Consumers often prefer salts perceived as less processed, mineral-rich, additive-free, or naturally harvested. However, suppliers must avoid exaggerated health claims and focus on authentic product attributes such as texture, source, flavor, harvesting method, and culinary performance.

- Future market growth will be shaped by premium cooking, gourmet retail expansion, foodservice innovation, flavored salt blends, artisanal sourcing, e-commerce specialty foods, sustainable packaging, and demand for visually distinctive ingredients. Companies offering consistent quality, attractive packaging, traceable sourcing, strong culinary positioning, and application-specific salt formats are expected to remain competitive.

Market Scope

| Parameter | Gourmet Salt Market Detail |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Application, and By Distribution Channel |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Claim

- Organic

- Sodium Free/Low Sodium

- Conventional

By Type

- Sel Gris

- Flakey Salt

- Himalayan Salt

- Fleur de sel

- Specialty Salt

- Others

By Application

- Bakery

- Confectionary

- Meat & Poultry

- Sea Food

- Sauces & Savories

- Others

By Distribution Channel

- Direct

- Retail

- Online

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

- Cargill, Inc.

- SaltWorks, Inc.

- Morton Salt, Inc.

- Maldon Salt Company Limited

- Murray River Salt

- Amagansett Sea Salt Co.

- Alaska Pure Sea Salt Co.

- Jacobsen Salt Co.

- Le Saunier de Camargue

- San Francisco Salt Company

- Salt Traders

- The Savory Pantry

- Bitterman Salt Co.

Recent Developments

May 2026 – Maldon Salt launched new 50g flavoured sea salt tubs for Garlic, Chilli, and Pepper variants. The compact resealable format was positioned for everyday cooking, outdoor dining, barbecues, and convenient premium seasoning, reinforcing demand for smaller-pack gourmet salts with stronger flavour-led positioning.

May 2026 – McCormick launched a new finishing salts and sugars range. The company introduced finishing salt flavours including Brown Butter, Ranch, Applewood Smoked Salt & Bacon, Honey Chipotle, Smoky Garlic & Rosemary, and Zesty Lemon, supporting the shift toward gourmet-style seasoning products for home cooks.

May 2026 – Saltverk expanded into the U.S. foodservice channel with restaurant-size flaky sea salt offerings. The move strengthened the company’s positioning among chefs, restaurants, and premium kitchens seeking sustainable Icelandic flaky sea salt produced using geothermal energy.

May 2026 – Saltverk’s Flaky Sea Salt Pouch was named a 2026 NEXTY Award finalist in the spices and condiments category. The recognition highlighted growing retail attention toward sustainable, premium, hand-harvested sea salt products and clean-label gourmet pantry ingredients.

November 2025 – Maldon Salt launched Pepper Sea Salt across Morrisons stores and online. The product combined Maldon’s hand-harvested sea salt flakes with Tellicherry and pink peppercorns, expanding the brand’s flavoured sea salt portfolio for premium everyday cooking and finishing applications.

October 2025 – Diamond Crystal introduced its first flavoured kosher salts. The new range included Lemon, Black Lime, and Sweet Heat variants, designed for seasoning, finishing, cocktail rimming, and culinary experimentation, reflecting the movement of chef-preferred salt brands into value-added flavour formats.

August 2025 – Saltverk expanded retail availability through Meijer. The distribution expansion supported wider U.S. access to Icelandic hand-harvested sea salt and highlighted growing retail demand for sustainable, origin-based gourmet salt products.

July 2025 – WHO updated its sodium reduction fact sheet, reinforcing public health pressure on salt categories. The guidance continued to emphasize sodium reduction as a cost-effective public health priority, which affects positioning across gourmet salts, finishing salts, seasoning blends, and foodservice salt applications.

FAQ's

The Gourmet Salt Market is estimated to reach USD 695.8 million by 2032.

The Global Gourmet Salt Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% during the forecast period from 2026 to 2032.

The Global Gourmet Salt Market is estimated to generate USD 481 million in revenue in 2026.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!