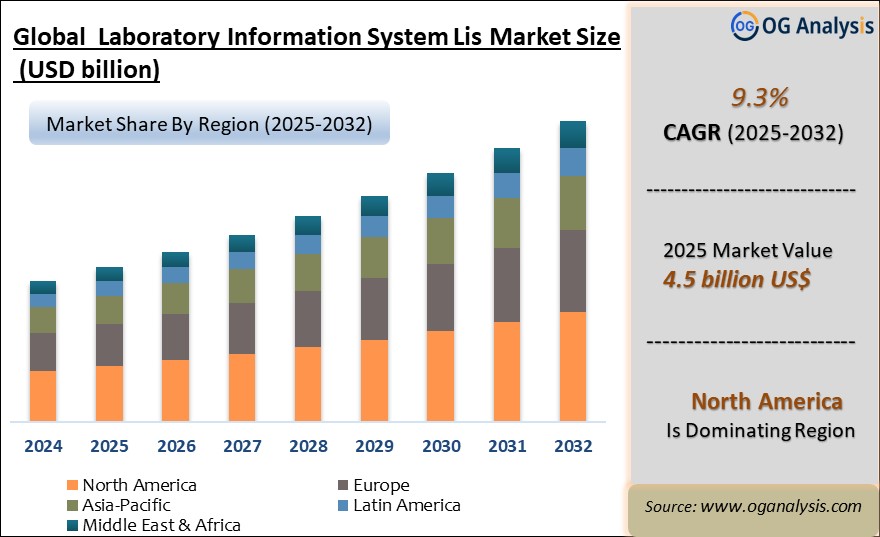

"The Laboratory Information System (LIS) Market Size was valued at USD 4.1 billion in 2024 and is projected to reach USD 4.5 billion in 2025. Worldwide sales of Laboratory Information System (LIS) are expected to grow at a significant CAGR of 9.3%, reaching USD 10.1 billion by the end of the forecast period in 2034."

Laboratory Information System (LIS) Market Overview

The Laboratory Information System (LIS) market is experiencing significant growth, driven by the increasing demand for laboratory automation and the need for efficient data management systems in healthcare and research settings. LIS are software systems designed to manage medical laboratory operations, data, and information more effectively. With the healthcare industry increasingly focused on precision and personalized medicine, LIS plays a critical role in enhancing the efficiency of laboratory processes by ensuring accurate data management and streamlined laboratory operations. The integration of LIS helps in managing complex data flows and supports regulatory compliance, contributing to enhanced diagnostic and research outputs.

Amidst the backdrop of a global push towards digital health solutions, LIS have become indispensable in modern medical infrastructures. They not only facilitate seamless integration of laboratory services with electronic health records (EHR) but also improve the quality and speed of laboratory testing. As laboratories face growing pressure to deliver faster and more accurate results, the adoption of LIS is expected to proliferate. The market's expansion is further propelled by the rising prevalence of chronic diseases, which necessitates regular and sophisticated testing protocols that LIS systems are uniquely equipped to handle.

North America is the leading region in the Laboratory Information System (LIS) market, powered by advanced healthcare infrastructure, increasing adoption of digital health technologies, and a strong presence of key market players.

Clinical laboratories segment is the dominating segment in the LIS market, fueled by the rising demand for efficient diagnostic workflows, growing test volumes, and the need for streamlined laboratory operations.

Laboratory Information System (LIS) Market Latest Trends, Drivers and Challenges

One of the leading trends in the LIS market is the shift towards cloud-based solutions, offering scalability, remote access, and cost efficiency. Cloud-based LIS enable laboratories to manage operations without the need for extensive on-premise IT infrastructure, thus reducing capital expenditure and maintenance costs. Furthermore, the adoption of Artificial Intelligence (AI) and machine learning technologies in LIS is gaining momentum. These technologies enhance data analysis capabilities, enabling predictive analytics that can forecast trends, automate routine tasks, and provide deeper insights into laboratory processes. Another significant trend is the integration of LIS with mobile technologies, allowing healthcare providers to access laboratory results and manage tasks directly from their smartphones or tablets, thereby improving workflow efficiency and data accessibility.

The primary drivers of the LIS market include technological advancements in healthcare IT, growing emphasis on laboratory automation, and the increasing burden of chronic diseases. As healthcare providers seek to enhance operational efficiencies and patient outcomes, the deployment of advanced LIS becomes crucial. The regulatory environment also plays a significant role in driving the adoption of LIS, as compliance with health data standards and practices is mandatory in many regions. Additionally, the surge in laboratory tests due to an aging population and the global increase in health awareness are pushing laboratories towards sophisticated systems like LIS to manage high volumes of data and improve turnaround times.

Despite the growth, the LIS market faces several challenges. High initial costs and complexities involved in implementing LIS can deter smaller laboratories and healthcare facilities from adopting the technology. Interoperability issues between different healthcare IT systems, including EHRs and LIS, pose another significant challenge, as seamless data exchange is crucial for effective operations. Data security concerns, particularly with cloud-based systems, also impede market growth, as laboratories handle sensitive patient information that must be protected against breaches. Furthermore, there is a persistent skill gap in healthcare IT, necessitating continuous training and development to effectively operate and manage advanced LIS solutions.

Regional Insights

North America

North America’s LIS market is driven by mature clinical laboratory networks, high test volumes, strict quality and audit requirements, and strong demand for automation and interoperability across hospital labs, reference labs, and integrated delivery networks. Market dynamics emphasize consolidation of multi-site lab operations, standardization of workflows, and tight integration with EHRs, billing, and analytics to reduce turnaround time and errors. Lucrative opportunities are strongest in enterprise LIS modernization, cloud and hybrid migration programs, middleware connectivity for instruments and automation tracks, and advanced modules for microbiology, molecular diagnostics, and blood bank/transfusion workflows. Latest trends include API-first interoperability, cybersecurity hardening, automation-friendly LIS architectures, and embedded analytics for workload balancing and utilization management. The forecast remains positive as laboratories replace legacy systems, expand outreach testing, and adopt scalable platforms that support both routine and specialized testing, while recent developments highlight vendor partnerships and platform expansions that unify LIS with broader lab operations and revenue-cycle workflows.

Asia Pacific

Asia Pacific’s LIS market is expanding rapidly due to healthcare digitization, growth in private diagnostics chains, rising chronic disease testing, and increasing regulatory focus on traceability and lab quality across diverse health systems. Market dynamics differ by country but commonly center on scalable deployment, multi-language and multi-site support, and cost-effective configurations that can integrate with heterogeneous hospital IT environments and a wide range of instruments. Lucrative opportunities include greenfield implementations for fast-growing diagnostic networks, cloud-enabled LIS for mid-tier hospitals and independent labs, and specialized capabilities for molecular testing, pathology connectivity, and public health reporting. Trends include mobile-enabled sample collection workflows, tighter integration with laboratory automation, and adoption of analytics to improve productivity in high-growth labs. The forecast is strong as regional lab networks expand and standardize operations, with recent developments focusing on modular rollouts, cloud adoption where permitted, and interoperability improvements to support cross-facility care and centralized reporting.

Europe

Europe’s LIS market is shaped by stringent data privacy, mature quality frameworks, and increasing pressure to improve efficiency amid workforce constraints and rising demand for diagnostic services. Market dynamics prioritize interoperability with national and regional health infrastructures, standardized coding and reporting, and robust audit trails to support accreditation and compliance. Lucrative opportunities are concentrated in cross-border and multi-country lab groups, enterprise harmonization projects that unify disparate legacy LIS instances, and solutions that support automation, digital workflows, and integrated analytics for capacity planning and turnaround optimization. Latest trends include cloud and hybrid models aligned with sovereignty requirements, stronger cybersecurity controls, and workflow digitization for microbiology and molecular testing. The forecast is steady as laboratories modernize platforms and consolidate operations, while recent developments emphasize platform unification, improved interface management, and tighter integration of LIS with scheduling, logistics, and clinical decision support.

Middle East & Africa

Middle East & Africa is driven by hospital expansion, private diagnostics growth, and national digital health initiatives that are increasing the need for standardized laboratory operations and reliable connectivity across distributed facilities. Market dynamics highlight the importance of turnkey implementations, strong local service and integration partners, and solutions that can operate effectively in mixed infrastructure environments while meeting accreditation and reporting requirements. Lucrative opportunities are strongest in new hospital projects, centralized reference lab models, and large diagnostic networks seeking consistent sample tracking, quality controls, and faster turnaround times. Trends include increasing adoption of cloud-hosted or centrally managed deployments where feasible, stronger instrument connectivity and automation integration, and rising demand for patient-facing result portals and secure data exchange. The forecast is favorable as healthcare capacity grows and lab networks professionalize, with recent developments centered on enterprise standardization, connectivity upgrades, and stronger compliance and security frameworks.

South & Central America

South & Central America’s LIS market is influenced by expanding private diagnostics, modernization of public health systems, and the need to improve efficiency and traceability in laboratories operating under cost constraints and variable IT maturity. Market dynamics emphasize interoperability, phased modernization, and strong workflow controls that reduce manual errors and improve sample-to-result visibility across multi-site networks. Lucrative opportunities include upgrades from legacy systems, enterprise harmonization for regional diagnostic chains, integration with billing and claims processes, and modules that support microbiology, molecular testing, and outreach lab programs. Latest trends include broader adoption of cloud and managed services, increased focus on cybersecurity and access control, and analytics to reduce rework and optimize staffing and instrument utilization. The forecast is steady to positive as lab networks scale and standardize, with recent developments focused on modular deployments, improved instrument connectivity, and integration with broader hospital and public health information systems.

Market Scope

| Parameter | Laboratory Information System (LIS) Market Scope Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Product Type, By Diagnostic Method, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product:

- Standalone LIS

- Integrated LIS

By Component:

- Services

- Software

By End User:

- Hospitals and Clinics

- Independent Laboratories

- Others

By Geography:

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

1. Cerner Corporation

2. McKesson Corporation

3. Sunquest Information Systems Inc.

5. Medical Information Technology, Inc. (Meditech)

6. Compugroup Medical

7. Computer Programs and Systems, Inc. (CPSI)

8. Merge Healthcare, Inc.

9. Orchard Software Corporation

10. STARLIMS Corporation

11. Thermo Fisher Scientific Inc.

12. SCC Soft Computer

13. Sysmex Corporation

14. LabWare

15. LabVantage Solutions, Inc.

Recent Industry Developments

-

Jan 2026 – Oracle Health Sciences: Announced integration enhancements between Oracle’s clinical data platforms and LIS workflows, aiming to improve interoperability, streamline lab data exchange, and support more unified electronic health record (EHR) connectivity for healthcare providers.

-

Dec 2025 – LabWare: Launched LabWare 8.0 with a renewed focus on cloud-native deployment options, expanded automation integration, and advanced analytics tools to improve lab operations, compliance tracking, and workflow customization.

-

Nov 2025 – Abbott Diagnostics: Announced expanded interoperability between Alinity LIS interfaces and third-party hospital systems, enhancing real-time data sharing and reducing manual result entry for improved turnaround times.

-

Oct 2025 – Sunquest Information Systems: Released major updates to its Sunquest LIS platform with enhanced genomics and molecular diagnostics modules, designed to better support high-complexity testing workflows and structured data reporting.

-

Sep 2025 – Roche Diagnostics: Introduced new middleware integrations between its lab analyzers and external LIS platforms to standardize result flows and reduce integration complexity for clinical labs adopting hybrid instrument fleets.

-

Jul 2025 – CompuGroup Medical (CGM): Announced platform enhancements that extend CGM LIS connectivity with population health systems and value-based care analytics, positioning LIS data for broader clinical insights and care coordination.

-

Jun 2025 – Cerner/Labs at Oracle: Following the acquisition of Cerner by Oracle, Oracle Health confirmed migration pathways for legacy Cerner lab systems into Oracle’s unified LIS/EHR ecosystem, supporting continuity for existing clients.

FAQ's

The Laboratory Information System (LIS) Market is estimated to reach USD 8.4 billion by 2032.

The Global Laboratory Information System (LIS) Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 9.3% during the forecast period from 2025 to 2032.

The Global Laboratory Information System (LIS) Market is estimated to generate USD 4.1 billion in revenue in 2024.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!