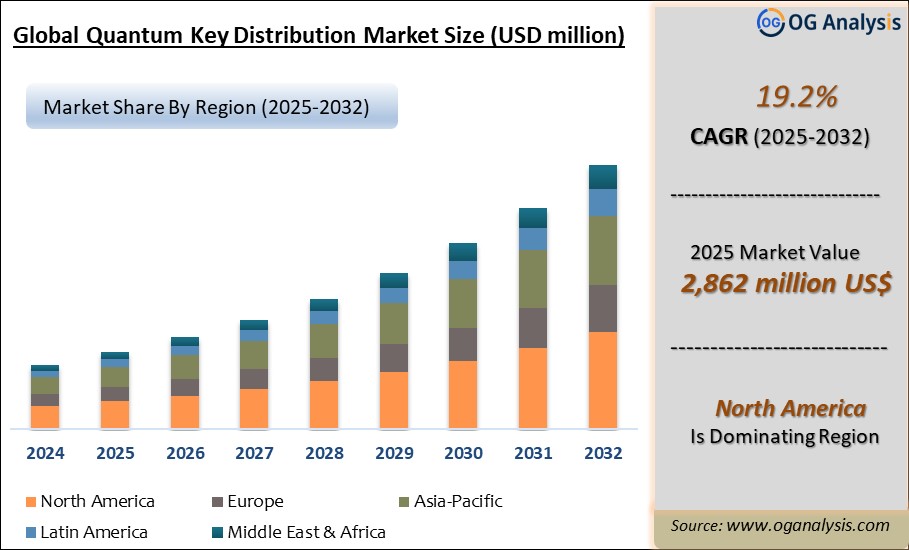

""The Quantum Key Distribution Market valued at $ 2,401. Million in 2024, is expected to grow by 19.2% CAGR to reach market size worth $ 14,196.5 Million by 2034.""

The Quantum Key Distribution (QKD) market is an emerging and rapidly growing segment within the global cybersecurity and cryptography landscape. QKD leverages the principles of quantum mechanics to enable secure communication by allowing two parties to exchange encryption keys in a way that any eavesdropping attempts are detected immediately. This unique feature stems from the quantum property of "quantum entanglement," which ensures that any interception of data will disturb the system, thereby alerting the communicating parties. As global concerns about data security intensify due to the rise in cyberattacks, data breaches, and the advent of quantum computing, QKD is gaining traction as a potential solution to ensure ultra-secure communication networks. The market is expected to grow significantly as more industries, especially in finance, government, healthcare, and telecommunications, adopt quantum cryptography technologies to safeguard sensitive data from future threats posed by quantum computers. Additionally, government initiatives and strategic investments are further driving innovation in QKD, creating opportunities for private players to develop commercial solutions. While the technology is still in its nascent stages, QKD's potential for providing virtually unbreakable encryption is poised to revolutionize the cybersecurity landscape over the coming years.

The Quantum Key Distribution market is poised to see rapid expansion, driven by the increasing demand for secure communication technologies in an era of growing cyber threats. Innovations in quantum cryptography, combined with investments from government agencies and private enterprises, are propelling the development of QKD systems. These systems are expected to be crucial in protecting sensitive information, especially as quantum computing continues to advance. The market is also witnessing collaborations between academia, research institutions, and private companies to create scalable, real-world QKD solutions. These partnerships aim to make QKD commercially viable, addressing challenges like high costs, complex infrastructure requirements, and the need for new protocols to integrate quantum and classical systems. North America, Europe, and parts of Asia-Pacific are expected to be the leading regions for QKD adoption, with significant advancements in quantum research and infrastructure. However, the high cost of deployment and the need for further technological advancements in quantum repeaters and photon detection remain challenges that the market must overcome. Nevertheless, the growing awareness of quantum security's importance and the potential for post-quantum encryption are expected to drive widespread implementation of QKD systems in the next decade.

By component, solution is the largest segment in the Quantum Key Distribution market. The demand for QKD solutions is driven by the need for secure communication across various industries, particularly in sectors like finance, government, and healthcare. These solutions offer end-to-end encryption capabilities that protect sensitive data, making them the preferred choice for organizations seeking high-level cybersecurity.

By type, extended range communication systems is the fastest-growing segment in the Quantum Key Distribution market. As the need for secure communication over longer distances increases, extended range systems offer a solution by overcoming the distance limitations inherent in traditional QKD technologies. These systems are essential for large-scale deployment in sectors such as government communications and international financial transactions.

Quantum Key Distribution Market Strategy, Price Trends, Drivers, Challenges and Opportunities to 2034

-

The QKD market is rapidly expanding due to the growing need for ultra-secure communication, driven by rising cyberattacks and the potential threats posed by quantum computing. Industries like finance, government, and healthcare are particularly focused on adopting quantum cryptography.

-

QKD leverages quantum mechanics, specifically quantum entanglement, to securely exchange encryption keys, making it nearly impossible for eavesdropping to go undetected. This innovative technology offers virtually unbreakable encryption, providing significant advancements in cybersecurity.

-

Governments and enterprises are investing in quantum cryptography to future-proof their cybersecurity systems against the potential risks posed by quantum computers. These investments are accelerating QKD adoption across key sectors, ensuring long-term security for sensitive data.

-

Quantum Key Distribution systems are still in early development but show tremendous potential for widespread implementation in the coming years. As research and development progress, QKD is expected to become a mainstream solution for secure communications.

-

The integration of QKD into current communication networks presents challenges, such as the high cost of implementation, the need for new infrastructure, and the complexity of creating hybrid quantum-classical systems. However, these barriers are being addressed through technological advancements and collaborations.

-

North America and Europe are leading the QKD market, supported by robust government-backed initiatives and investments in quantum research. Asia-Pacific is also seeing rapid developments, particularly in China, which has made significant strides in quantum computing and cryptography.

-

The finance and telecommunications sectors are key early adopters of QKD, where the protection of sensitive transactions and communications is a top priority. These sectors recognize the potential of QKD to provide long-term security against evolving cyber threats.

-

The development of quantum repeaters, essential for overcoming the distance limitations of QKD systems, is one of the major areas of innovation. Progress in this field is critical for scaling QKD systems for broader use across large geographical areas.

-

Quantum Key Distribution is expected to play a critical role in the development of post-quantum cryptography solutions, ensuring that data remains secure even after quantum computers become capable of breaking traditional encryption algorithms.

-

QKD’s potential for providing secure communication is attracting a wide range of players in the cybersecurity space, including academic researchers, technology companies, and government organizations, all collaborating to push forward the commercialization of quantum cryptography solutions.

North America Quantum Key Distribution Market Analysis

The North American Quantum Key Distribution market experienced significant advancements in 2024, driven by the increasing adoption of smart technologies along with investments in innovation. Key developments included accelerated integration of manufacturing processes, breakthroughs in novel technologies, and advancements in AI-powered product development. The region’s dominance stems from substantial defense budgets, a robust R&D ecosystem, and the presence of leading market players such as Lockheed Martin, Boeing, and Raytheon Technologies. From 2025, the market is projected to grow steadily, fueled by the rising demand for hypersonic weapons, autonomous aircraft, and quantum communication technologies. Supporting factors include government initiatives to modernize defense infrastructure, the rapid expansion of satellite communication networks, and advancements in green aviation technologies. A competitive landscape marked by innovation and strategic collaborations ensures that North America remains at the forefront of the Quantum Key Distribution market.

Europe Quantum Key Distribution Market Outlook

In 2024, Europe’s Quantum Key Distribution market witnessed pivotal technological developments, and increased investments in sustainable solutions, bolstered by EU green initiatives. The European Quantum Key Distribution market is expected to thrive from 2025, supported by a strong focus on the modernization of systems, and the deployment of advanced mobility solutions. Factors such as regional collaboration through NATO, the European Space Agency (ESA) programs, and funding for advanced avionics systems are key growth drivers in the broader perspective. The competitive landscape is shaped by major players like Airbus, Thales Group, and Leonardo S.p.A., leveraging cutting-edge technology and partnerships to enhance capabilities across sectors.

Asia-Pacific Quantum Key Distribution Market Forecast

Asia-Pacific emerged as a dynamic region for the Quantum Key Distribution market in 2024, with key developments in strategic segments. Rapidly growing defense budgets in China and India, coupled with technological innovation in Japan and South Korea, are propelling market growth. From 2025, the market is anticipated to expand significantly due to escalating geopolitical tensions, increased investment in commercial satellite communications, and urban air mobility projects in megacities. Factors such as government-backed aerospace programs, rising adoption of AI in defense systems, and the region's push toward localized manufacturing amplify growth from a broader purview. The competitive landscape features global giants like Boeing and Lockheed Martin alongside regional powerhouses such as Hindustan Aeronautics Limited (HAL) and Mitsubishi Electric.

Middle East, Africa, Latin America Quantum Key Distribution Market Overview

The Middle East, Africa, Latin America Quantum Key Distribution market, encompassing the Middle East, Africa, and South America, saw noteworthy progress in 2024. Countries like Saudi Arabia and the UAE led in defense modernization, while Brazil and South Africa focused on commercial aviation and satellite communications are growth engines in Aerospace and Defence segment. Anticipated growth from 2025 is underpinned by rising defense expenditure, increasing space exploration activities, and the adoption of advanced avionics systems. Supporting factors include strategic international partnerships, growing demand for smart weapons, and investments in airport logistics systems. The Quantum Key Distribution market remains highly competitive, with key players forming joint ventures and leveraging advanced technologies to meet regional demands. The RoW market holds immense potential for growth as nations focus on bolstering their capabilities.

Quantum Key Distribution Market Dynamics and Future Analytics

The research analyses the Quantum Key Distribution parent market, derived market, intermediaries’ market, raw material market, and substitute market are all evaluated to better prospect the Quantum Key Distribution market outlook. Geopolitical analysis, demographic analysis, and Porter’s five forces analysis are prudently assessed to estimate the best Quantum Key Distribution market projections.

Recent deals and developments are considered for their potential impact on Quantum Key Distribution's future business. Other metrics analyzed include the Threat of New Entrants, Threat of New Substitutes, Product Differentiation, Degree of Competition, Number of Suppliers, Distribution Channel, Capital Needed, Entry Barriers, Govt. Regulations, Beneficial Alternative, and Cost of Substitute in Quantum Key Distribution market.

Quantum Key Distribution trade and price analysis helps comprehend Quantum Key Distribution's international market scenario with top exporters/suppliers and top importers/customer information. The data and analysis assist our clients in planning procurement, identifying potential vendors/clients to associate with, understanding Quantum Key Distribution price trends and patterns, and exploring new Quantum Key Distribution sales channels. The research will be updated to the latest month to include the impact of the latest developments such as the Russia-Ukraine war on the Quantum Key Distribution market.

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD million |

| Market Splits Covered | By Product, By Application and By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Quantum Key Distribution Market Segmentation

by Component

- Solution

- Services

by Type

- Extended Range Communication Systems

- Multiplexing Transmission Systems

by Application

- Secure Communication

- Network Security

- Database Encryption

by End-user

- Government and Defense

- Healthcare

- IT and Telecom

- Automotive

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Playes

-

ID Quantique

-

InfiniQuant

-

KETS Quantum Security

-

Kloch

-

LuxQuanta

-

MagiQ Technologies

-

NEC

-

QuintessenceLabs

-

Telsy

-

Toshiba

Recent Developments

In July 2025, IonQ completed the acquisition of Capella Space, aiming to develop the world's first space-based quantum key distribution network. This integration combines Capella's satellite infrastructure with IonQ's quantum technology to enable secure communications and expand quantum networking capabilities.

In May 2025, SEALSQ Corp announced a $10 million investment in WISeSat.Space to accelerate the deployment of a satellite constellation for space-based quantum key distribution. This initiative focuses on providing ultra-secure communications and decentralized IoT transactions through a quantum-resilient satellite network.

In April 2025, MicroCloud Hologram Inc. proposed a high-dimensional quantum key distribution protocol utilizing quantum Fourier transform and quantum-controlled NOT gate operations. This innovative approach enhances security and information efficiency in quantum transmission, positioning the company at the forefront of quantum key distribution technology development.

In March 2025, scientists at IIT Delhi demonstrated a trusted-node-free quantum key distribution over a distance of 380 km using standard telecom fiber, achieving a low quantum bit error rate. This advancement marks a significant step towards practical and scalable quantum communication systems.

In February 2025, researchers from Oxford University experimentally demonstrated the distribution of quantum computations between two photonically interconnected trapped-ion modules, achieving deterministic teleportation of a controlled-Z gate with 86% fidelity. This milestone represents progress toward scalable quantum computing and the development of a quantum internet.

In January 2025, IonQ announced plans to launch a global space-based quantum key distribution network by acquiring Capella Space. This acquisition aims to integrate Capella's satellite infrastructure with IonQ's quantum technology to enable secure communications and extend quantum networking capabilities.

In December 2024, the Indian startup QpiAI launched a 25-qubit superconducting quantum computer named QpiAI-Indus, marking a significant advancement in India's quantum computing capabilities. This development is part of the country's broader efforts to enhance its position in the global quantum technology landscape.

In November 2024, Toshiba Digital Solutions and KT demonstrated a hybrid quantum-secure communication system in South Korea. This demonstration integrated quantum key distribution with post-quantum cryptography, aligning with South Korea's national roadmap to promote quantum-resistant cryptography.

In October 2024, lyntia partnered with ID Quantique, Nokia, LuxQuanta, evolutionQ, OFS, and Digital Realty to conduct a pioneering quantum key distribution test using hollow core fiber-optic technology. This collaboration aimed to enhance data center security and interoperability between QKD manufacturers.

In September 2024, Sparkle, Telsy, and Quantum Telecommunications Italy collaborated to demonstrate quantum key distribution on a high-capacity link in Athens. This initiative showcased quantum-secured connectivity over existing networks to enhance data protection against future cyber threats.

Who can benefit from this research

The research would help top management/strategy formulators/business/product development/sales managers and investors in this market in the following ways

1. The report provides 2024 Quantum Key Distribution market sales data at the global, regional, and key country levels with a detailed outlook to 2034 allowing companies to calculate their market share and analyze prospects, uncover new markets, and plan market entry strategy.

2. The research includes the Quantum Key Distribution market split into different types and applications. This segmentation helps managers plan their products and budgets based on the future growth rates of each segment

3. The Quantum Key Distribution market study helps stakeholders understand the breadth and stance of the market giving them information on key drivers, restraints, challenges, and growth opportunities of the market and mitigating risks

4. This report would help top management understand competition better with a detailed SWOT analysis and key strategies of their competitors, and plan their position in the business

5. The study assists investors in analyzing Quantum Key Distribution business prospects by region, key countries, and top companies' information to channel their investments.

Available Customizations

The standard syndicate report is designed to serve the common interests of Quantum Key Distribution Market players across the value chain and include selective data and analysis from entire research findings as per the scope and price of the publication.

However, to precisely match the specific research requirements of individual clients, we offer several customization options to include the data and analysis of interest in the final deliverable.

Some of the customization requests are as mentioned below –

Segmentation of choice – Our clients can seek customization to modify/add a market division for types/applications/end-uses/processes of their choice.

Quantum Key Distribution Pricing and Margins Across the Supply Chain, Quantum Key Distribution Price Analysis / International Trade Data / Import-Export Analysis,

Supply Chain Analysis, Supply – Demand Gap Analysis, PESTLE Analysis, Macro-Economic Analysis, and other Quantum Key Distribution market analytics

Processing and manufacturing requirements, Patent Analysis, Technology Trends, and Product Innovations

Further, the client can seek customization to break down geographies as per their requirements for specific countries/country groups such as South East Asia, Central Asia, Emerging and Developing Asia, Western Europe, Eastern Europe, Benelux, Emerging and Developing Europe, Nordic countries, North Africa, Sub-Saharan Africa, Caribbean, The Middle East and North Africa (MENA), Gulf Cooperation Council (GCC) or any other.

Capital Requirements, Income Projections, Profit Forecasts, and other parameters to prepare a detailed project report to present to Banks/Investment Agencies.

Customization of up to 10% of the content can be done without any additional charges.

Note: Latest developments will be updated in the report and delivered within 2 to 3 working days

FAQ's

The Quantum Key Distribution Market is estimated to reach USD 14,196.5 Million by 2034.

The Global Quantum Key Distribution Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 19.2% during the forecast period from 2025 to 2034.

The Global Quantum Key Distribution Market is estimated to generate USD 2,833.4 Million in revenue in 2025

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!