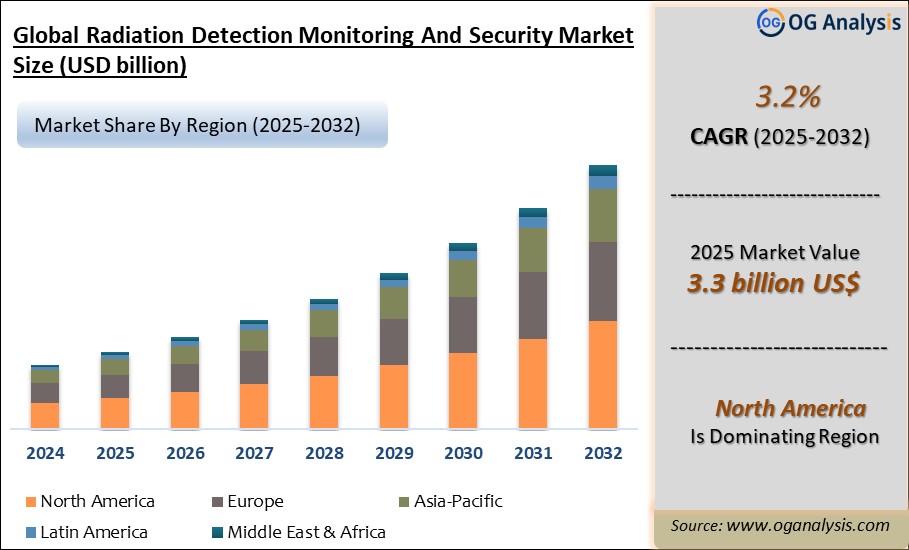

"The Global Radiation Detection Monitoring and Security Market is valued at USD 3.2 billion in 2024 and is projected to reach USD 3.3 billion in 2025. Worldwide sales of Radiation Detection Monitoring and Security are expected to grow at a significant CAGR of 3.2%, reaching USD 4.38 billion by the end of the forecast period in 2034."

"Rising Global Security Concerns and Technological Advancements Fuel Growth in the Radiation Detection, Monitoring, and Security Market"

The Radiation Detection, Monitoring, and Security Market has gained significant momentum in recent years, driven by increasing concerns over safety and security across a variety of industries. The need for radiation detection is critical in areas such as nuclear power plants, medical facilities, homeland security, and environmental monitoring. In 2024, the market witnessed steady growth, primarily due to heightened global security concerns, the expansion of nuclear energy projects, and the increased use of radiation-based technology in healthcare. Advanced radiation detection and monitoring technologies are playing a pivotal role in ensuring safety by identifying hazardous radiation levels and preventing exposure in sensitive environments.

Looking forward to 2025, the Radiation Detection, Monitoring, and Security Market is expected to continue its upward trajectory, driven by technological advancements and increased government regulations on radiation safety. Growing awareness of the dangers of radiation exposure, especially in developing regions, will contribute to market growth. Furthermore, the rising demand for advanced radiation detection devices in medical imaging, cancer treatment, and diagnostics is expected to fuel innovation and market expansion. As governments and regulatory bodies continue to enforce stringent safety protocols, the need for reliable radiation detection solutions across industries will become increasingly important, shaping the market„¢s future growth.

North America is the leading region in the Radiation Detection Monitoring and Security Market, powered by advanced healthcare infrastructure, significant nuclear energy investments, and stringent radiation safety regulations.

Radiation Detection, Monitoring, and Security Market Latest Trends

The Radiation Detection, Monitoring, and Security Market is evolving, with several emerging trends that are shaping its growth. One key trend is the increasing use of radiation detection devices in the healthcare sector. With the expansion of medical imaging technologies such as X-rays, CT scans, and radiotherapy, healthcare providers are increasingly investing in advanced radiation detection solutions to ensure patient and staff safety. In 2024, significant advancements in portable and wearable radiation detection devices have enabled healthcare workers to monitor exposure levels in real-time, minimizing risks and improving safety protocols. These innovations are expected to gain further traction as medical radiation usage continues to rise globally.

Another trend influencing the market is the integration of radiation detection systems with IoT (Internet of Things) and artificial intelligence (AI) technologies. In industries such as nuclear energy and homeland security, smart radiation monitoring systems are becoming increasingly popular. These systems can collect, analyze, and report data in real-time, allowing for more efficient detection and response to radiation threats. AI-powered systems are also improving the accuracy and reliability of radiation detection by minimizing false alarms and enhancing predictive maintenance capabilities. As these technologies advance, they will play a crucial role in improving the efficiency of radiation detection and monitoring systems.

Radiation Detection, Monitoring, and Security Market Drivers

Several factors are expected to drive the future growth of the Radiation Detection, Monitoring, and Security Market. One of the primary drivers is the expansion of nuclear power plants worldwide. With increasing energy demands and the global shift toward cleaner energy sources, nuclear power is gaining prominence. Radiation detection and monitoring solutions are essential in ensuring the safety of nuclear power plants and preventing the leakage of harmful radiation. Governments and regulatory bodies are imposing stricter regulations to safeguard both workers and the environment, which is expected to drive the demand for radiation detection solutions in the energy sector.

The healthcare industry is also a major driver of the market, with the rising use of radiation in diagnostics and treatment procedures. As cancer rates rise globally, the use of radiation-based therapies, such as radiotherapy, is expected to increase, further driving the need for effective radiation monitoring solutions. Additionally, increasing investments in research and development by medical device manufacturers will likely result in new and improved radiation detection technologies. The military and defense sectors are also expected to contribute to market growth, with heightened concerns over nuclear terrorism and the need for robust radiation detection systems in border security, military bases, and critical infrastructure.

Radiation Detection, Monitoring, and Security Market Challenges

Despite the promising growth prospects, the Radiation Detection, Monitoring, and Security Market faces several challenges. One of the most significant challenges is the high cost of advanced radiation detection systems. Although these systems provide essential safety benefits, the high price tags can deter small and medium-sized enterprises (SMEs) and healthcare facilities from adopting the latest technologies. In cost-sensitive markets, companies may struggle to justify the investment, especially in industries where radiation exposure risks are perceived as lower. Another challenge is the complexity of operating advanced radiation detection devices, which require specialized training and expertise. This can pose a barrier to widespread adoption, particularly in developing regions where technical knowledge may be limited.

In addition to cost and complexity, the market also faces regulatory hurdles. Different regions have varying standards and regulations regarding radiation safety, which can complicate the global distribution of radiation detection products. Manufacturers must navigate these regulatory landscapes carefully, ensuring compliance with international standards while tailoring products to meet local requirements. Furthermore, the risk of cyber threats to radiation monitoring systems is an emerging concern, as digital systems become more integrated with IoT and AI technologies. Ensuring the cybersecurity of these systems will be critical to their long-term success.

Competitive Landscape and Key Strategies

The competitive landscape of the Radiation Detection, Monitoring, and Security Market is characterized by the presence of several global players who are investing heavily in research and development to innovate and enhance their product offerings. Companies are focusing on developing portable, user-friendly, and cost-effective radiation detection devices to cater to a broader range of industries. Strategic collaborations and partnerships with healthcare providers, government agencies, and nuclear power plant operators are becoming increasingly common, allowing companies to expand their market presence and offer integrated solutions for radiation monitoring.

Leading players are also emphasizing sustainability by developing eco-friendly radiation detection devices with lower energy consumption. Additionally, as the market becomes more competitive, companies are adopting mergers and acquisitions as key strategies to strengthen their portfolios and expand their geographical reach. With the integration of AI, IoT, and machine learning into radiation detection technologies, companies are striving to improve product performance and reliability, ensuring long-term growth in the market. E-commerce platforms and digital marketing strategies are being leveraged to reach new customers and streamline product distribution globally.

Market Players

Key companies operating in the Radiation Detection, Monitoring, and Security Market include:

1. Thermo Fisher Scientific Inc.

2. Mirion Technologies Inc.

3. Landauer Inc.

4. Ludlum Measurements Inc.

5. FLIR Systems Inc.

6. Smiths Group plc

7. General Electric Company

8. Canberra Industries Inc.

9. Radiation Detection Company

10. Rapiscan Systems

11. Arrow-Tech Inc.

12. Polimaster Ltd.

13. RAE Systems Inc.

14. Kromek Group plc

15. Bertin Instruments

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD Billion |

| Market Splits Covered | By Product, By Composition, By End User, and By Equipment |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

By Product

- Radiation Detection & Monitoring Products

- Radiation Safety Products

By Composition

- Gas-filled Detectors

- Scintillators

- Solid-state Detectors

By End User

- Medical and Healthcare

- Industrial

- Homeland Security and Defense

- Energy and Power

- Other End User Industries

By Equipment

- Personal Dosimeters

- Area Process Monitors

- Environmental Radiation Monitor

- Surface Contamination Monitor

- Radioactive Material Monitor

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Global Radiation Detection Monitoring and Security Market is estimated to generate USD 3.2 billion in revenue in 2024.

The Global Radiation Detection Monitoring and Security Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 3.2% during the forecast period from 2025 to 2032.

The Radiation Detection Monitoring and Security Market is estimated to reach USD 4.1 billion by 2032.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!