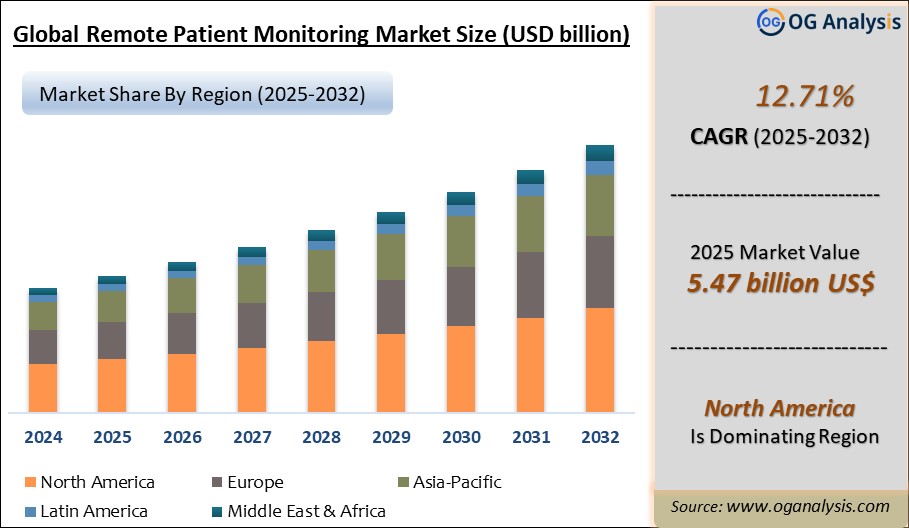

"The Remote Patient Monitoring Market is estimated to be USD 4.86 billion in 2024. Furthermore, the market is expected to grow to USD 11.2 billion by 2031, with a Compound Annual Growth Rate (CAGR) of 12.71%."

Remote Patient Monitoring Market Overview

The remote patient monitoring (RPM) market is experiencing substantial growth, driven by technological advancements in telehealth and an increasing emphasis on patient-centered care. RPM involves the use of digital technologies to monitor and capture medical and other health data from patients remotely and securely transmit this information to healthcare providers for assessment. This method is becoming particularly valuable for managing chronic diseases, post-operative care, and elderly care, allowing continuous monitoring without the need for patients to stay in the hospital. The market's expansion is further fueled by healthcare systems striving to reduce costs and improve the efficiency of healthcare delivery by minimizing hospital readmissions and visits.

The rising prevalence of chronic diseases worldwide, such as diabetes, cardiovascular diseases, and respiratory disorders, has made the need for continuous monitoring more critical than ever. RPM not only facilitates this need but also enhances patient engagement and compliance by keeping patients informed about their health status. As populations age and healthcare infrastructure continues to integrate more digital solutions, remote patient monitoring is positioned as a critical tool in the future of healthcare, providing vital data that can be used to improve patient outcomes and streamline care processes.

Remote Patient Monitoring Market Latest Trends,Drivers,Challenges

One of the most significant trends in the RPM market is the integration of artificial intelligence (AI) and machine learning (ML) into monitoring devices and systems. AI and ML enhance the capabilities of RPM tools by providing advanced data analytics, which helps in predicting patient health deterioration before it becomes critical. Another emerging trend is the use of wearable technology in RPM. Wearables, such as smartwatches and fitness bands, are equipped with sensors that can track a variety of health indicators like heart rate, blood pressure, and oxygen levels, providing continuous patient monitoring in a non-invasive manner.

The adoption of cloud-based solutions in RPM is also on the rise. These platforms offer scalable options for data storage and analytics, which are essential for managing the large volumes of data generated by remote monitoring devices. Cloud-based systems enable real-time data access and sharing among healthcare providers, which is crucial for quick decision-making and effective patient management. Additionally, there is an increasing focus on mobile health applications that support RPM, offering patients and doctors platforms to communicate directly and securely while facilitating better management of health conditions through mobile devices.

The main drivers of the RPM market include the growing global geriatric population, which is more susceptible to chronic diseases and requires continual medical monitoring. The increase in healthcare costs is also propelling the adoption of RPM technologies as they are cost-effective alternatives to traditional patient care methods. Additionally, improvements in healthcare infrastructure, particularly in developing countries, and favorable government initiatives promoting digital health solutions are significant factors contributing to the expansion of the RPM market. The COVID-19 pandemic has particularly highlighted the value of RPM, accelerating its adoption as it enables the monitoring of patients without physical contact, thus reducing the risk of virus transmission.

Despite the growth, the RPM market faces challenges such as data privacy and security concerns. The transmission and storage of medical data require stringent security measures to prevent breaches, which can be costly and complex to implement. There is also a challenge in the integration of RPM systems with existing healthcare IT systems, which can be resistant to change due to high costs and complexities involved. Additionally, there is a need for continuous education and training for healthcare providers and patients to effectively use and trust RPM technologies. Patient resistance due to technology adoption barriers, especially among the elderly, can also hinder market growth.

Major Players in the Remote Patient Monitoring Market

1. Philips Healthcare

2. Medtronic plc

3. Boston Scientific Corporation

4. GE Healthcare

5. Abbott Laboratories

6. Omron Healthcare

7. Masimo Corporation

8. Biotelemetry Inc.

9. Honeywell Life Care Solutions

10. Biotronik SE & Co. KG

11. Nihon Kohden Corporation

12. St. Jude Medical

13. Welch Allyn

14. VitalConnect

15. ResMed

Market Scope

| Parameter | Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2032 |

| Market Size-Units | USD Billion |

| Market Splits Covered | By Type, By Application, and By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Market Segmentation

- By Type:

- Devices

- Software

- Services

- By Application:

- Cardiovascular Diseases

- Diabetes

- Respiratory Diseases

- Weight Management and Fitness Monitoring

- By End User:

- Residential

- Commercial

Get Free Sample

At OG Analysis, we understand the importance of informed decision-making in today's dynamic business landscape. To help you experience the depth and quality of our market research reports, we offer complimentary samples tailored to your specific needs.

Start Now! Please fill the form below for your free sample.

Why Request a Free Sample?

Evaluate Our Expertise: Our reports are crafted by industry experts and seasoned analysts. Requesting a sample allows you to assess the depth of research and the caliber of insights we provide.

Tailored to Your Needs: Let us know your industry, market segment, or specific topic of interest. Our free samples are customized to ensure relevance to your business objectives.

Witness Actionable Insights: See firsthand how our reports go beyond data, offering actionable insights and strategic recommendations that can drive your business forward.

Embark on your journey towards strategic decision-making by requesting a free sample from OG Analysis. Experience the caliber of insights that can transform the way you approach your business challenges.

FAQ's

The Remote Patient Monitoring Market is estimated to reach USD 12.7 billion by 2032.

The Global Remote Patient Monitoring Market is expected to grow at a Compound Annual Growth Rate (CAGR) of 12.71% during the forecast period from 2025 to 2032.

The Global Remote Patient Monitoring Market is estimated to generate USD 4.86 billion in revenue in 2024.

$4150- 30%

$6450- 40%

$8450- 50%

$2850- 20%

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!