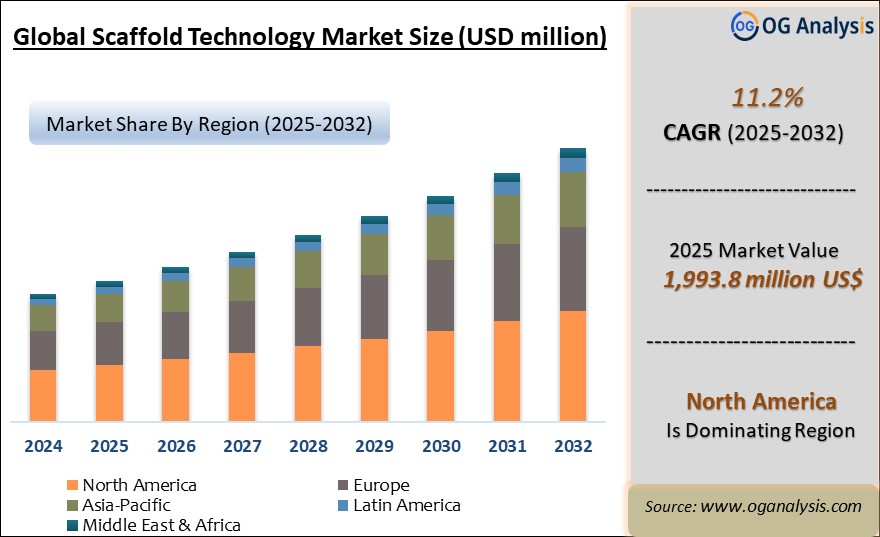

"The Scaffold Technology market, valued at $1,793.0 Million in 2024, is forecasted to grow at a CAGR of 11.2% to reach $5,292.4 Million by 2034."

The Scaffold Technology Market is witnessing robust growth driven by rising demand for regenerative medicine, tissue engineering, and 3D cell culture applications. Scaffold technologies provide a three-dimensional support structure for cells, enhancing cell adhesion, proliferation, and differentiation in various biomedical research and clinical practices. Increasing investments in stem cell research and advancements in biomaterials are fostering the development of novel scaffold designs. Applications span across pharmaceutical research, cancer biology, orthopedics, and wound healing, creating a multi-disciplinary commercial opportunity. Market players are focusing on biocompatible, biodegradable, and functionalized scaffolds to address therapeutic needs more effectively. The emergence of 3D bioprinting and hydrogel-based scaffolds is further accelerating market expansion. North America leads due to its strong R&D infrastructure and funding, while the Asia-Pacific region is experiencing significant growth, driven by increasing healthcare investments and academic collaborations.

Technological innovation, regulatory support for advanced therapies, and an increasing number of clinical trials using scaffold-based systems continue to shape the market dynamics. With a growing preference for in vitro models over animal testing, scaffold-based platforms are gaining traction in drug development pipelines. Moreover, partnerships among biotech firms, academic institutions, and research centers are facilitating the commercialization of scaffold-based products. As the field moves toward personalized medicine, scaffold technology is poised to play a vital role in disease modeling, drug screening, and organ regeneration research. Despite challenges related to scalability and standardization, the market outlook remains optimistic due to rising clinical translation of scaffold-based applications.

Nanofiber based scaffolds represent the fastest-growing segment by type, driven by their high surface area-to-volume ratio and ability to mimic natural extracellular matrices, which enhances cell attachment and proliferation for tissue engineering.

Bioresorbable materials lead the market by material, as their capacity to degrade safely in the body eliminates the need for surgical removal, making them highly attractive for regenerative medicine and implantable scaffold applications.

Orthopedics is the largest application segment due to the high prevalence of bone injuries and disorders, and the widespread use of scaffolds for bone grafts, repair, and regeneration in orthopedic procedures.

Key Insights

-

The increasing adoption of scaffold-based 3D cell cultures in pharmaceutical R&D is a key driver, offering better simulation of in vivo environments than traditional 2D cultures.

-

Hydrogel-based scaffolds are gaining popularity due to their high water content, biocompatibility, and similarity to natural extracellular matrices, making them ideal for tissue regeneration.

-

North America dominates the global scaffold technology market, supported by significant investments in regenerative medicine and a strong base of biopharmaceutical companies and research institutions.

-

Biodegradable polymer scaffolds are in high demand due to their ability to degrade naturally within the body, eliminating the need for surgical removal and minimizing side effects.

-

The orthopedic and musculoskeletal segment represents a major application area, with scaffolds being widely used for bone regeneration and cartilage repair.

-

3D bioprinting is transforming scaffold fabrication, allowing precise control over structure, porosity, and architecture, which enhances cell distribution and tissue integration.

-

Academic and clinical collaborations are fostering innovation, particularly in scaffold designs tailored for organ-specific regeneration such as liver, heart, and neural tissues.

-

Government grants and funding initiatives for stem cell and regenerative research are accelerating the development and adoption of scaffold technologies in clinical settings.

-

Scaffold-based in vitro models are increasingly replacing animal testing in toxicity and efficacy studies, aligning with ethical standards and regulatory preferences.

-

Challenges such as production cost, quality control, and scalability remain, but ongoing material science research is addressing these issues with promising outcomes.

Regional Insights

North America

North America’s scaffold technology market is driven by strong biopharmaceutical research, advanced tissue engineering programs, regenerative medicine initiatives, and a mature medical device ecosystem. Market dynamics emphasize biocompatibility, reproducibility, and regulatory alignment, as academic institutions, biotech firms, and contract research organizations seek reliable scaffold platforms for cell culture, organoid development, and translational therapies. Lucrative opportunities are strongest in 3D cell culture systems, stem cell expansion matrices, wound healing applications, and orthopedic and dental tissue regeneration solutions. Latest trends include growing use of bioresorbable polymers, hybrid natural-synthetic scaffold materials, and integration with bioprinting technologies to create more physiologically relevant models. The outlook remains positive as funding for regenerative medicine and personalized therapies continues, with recent developments focused on scalable manufacturing processes, improved porosity control, and partnerships between biomaterials suppliers and therapeutic developers.

Asia Pacific

Asia Pacific is witnessing rapid growth due to expanding life sciences research, increasing healthcare investment, and rising biotechnology and pharmaceutical manufacturing activity. Market dynamics prioritize cost-effective production, scalable biomaterial platforms, and technology transfer partnerships that accelerate commercialization. Lucrative opportunities lie in tissue engineering research, drug discovery screening models, regenerative therapies for orthopedic and cardiovascular applications, and collaboration-driven academic research programs. Trends include adoption of advanced polymer and collagen-based scaffolds, increasing integration with 3D bioprinting, and growing interest in nanofiber and hydrogel technologies that enhance cell adhesion and proliferation. The forecast remains robust as governments invest in biomedical innovation and local biotech ecosystems mature, with recent developments centered on research infrastructure expansion, regional manufacturing capabilities, and cross-border scientific collaborations.

Europe

Europe’s scaffold technology market is shaped by strong biomedical research networks, supportive regulatory frameworks for advanced therapies, and a growing focus on translational medicine. Market dynamics emphasize sustainability, ethical sourcing of biological materials, and compliance with stringent clinical and laboratory standards. Lucrative opportunities are concentrated in advanced wound care products, bone and cartilage regeneration scaffolds, organ-on-chip development, and personalized medicine platforms that rely on sophisticated 3D matrices. Latest trends include development of decellularized and bioactive scaffolds, incorporation of growth factors and bioactive molecules, and increased automation in scaffold fabrication processes. The outlook is steady to positive as regenerative medicine pipelines advance, with recent developments highlighting collaborative research consortia, innovation grants, and progress toward clinical-stage applications.

Middle East & Africa

Middle East & Africa represents an emerging market, driven by growing healthcare infrastructure, academic research expansion, and gradual investment in biotechnology capabilities. Market dynamics are influenced by import reliance, limited local biomaterial production, and the need for technology partnerships to build regional expertise. Lucrative opportunities exist in research-grade scaffolds for university laboratories, wound healing and orthopedic treatment solutions, and pilot regenerative medicine programs in advanced medical centers. Trends include increased collaboration with global biomaterials suppliers, gradual adoption of 3D cell culture models, and development of specialized research hubs. The outlook improves alongside healthcare modernization initiatives, with recent developments focusing on research funding growth, regional training programs, and strategic alliances to strengthen biomedical innovation capacity.

South & Central America

South & Central America’s scaffold technology market is supported by expanding university research, growing biotech startups, and rising demand for advanced medical treatments. Market dynamics emphasize affordability, dependable supply of research-grade materials, and partnerships that enable knowledge transfer and technical training. Lucrative opportunities are strongest in tissue engineering research, dental and orthopedic regenerative products, and drug discovery platforms utilizing 3D cell culture systems. Latest trends include adoption of collagen-based and biodegradable polymer scaffolds, increasing participation in international research collaborations, and gradual movement toward clinical translation of regenerative therapies. The outlook remains steadily positive as biomedical research ecosystems expand, with recent developments centered on improved distribution networks, capacity-building initiatives, and stronger engagement with global scaffold technology providers.

Reort Scope

| Parameter | Scaffold Technology Market Detail |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2026-2034 |

| Market Size-Units | USD billion |

| Market Splits Covered | By Type, By Material, By End User |

| Countries Covered | North America (USA, Canada, Mexico) |

| Analysis Covered | Latest Trends, Driving Factors, Challenges, Trade Analysis, Price Analysis, Supply-Chain Analysis, Competitive Landscape, Company Strategies |

| Customization | 10% free customization (up to 10 analyst hours) to modify segments, geographies, and companies analyzed |

| Post-Sale Support | 4 analyst hours, available up to 4 weeks |

| Delivery Format | The Latest Updated PDF and Excel Data file |

Segmentation

By Type

- Hydrogels

- Micropatterned Surface Microplates

- Nanofiber Based Scaffolds

By Material

- Bio-inert

- Bioresorbable

- Bioactive

- By Application

- Neurology

- Urology

- Orthopedics

- Dental

- Cardiology & Vascular

- Cancer

- Skin & Integumentary

- GI & Gynecology

- Others

By End-User

- Stem Cell Therapy, Tissue Engineering & Regenerative Medicine

- Drug Discover

- Others

By Geography

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

- Asia-Pacific (China, India, Japan, Australia, Vietnam, Rest of APAC)

- The Middle East and Africa (Middle East, Africa)

- South and Central America (Brazil, Argentina, Rest of SCA)

Key Market Players

-

Merck KGaA

-

Tecan Trading AG

-

3D Biotek LLC

-

Becton, Dickinson, and Company

-

Medtronic

-

Xanofi

-

Molecular Matrix, Inc.

-

Matricel GmbH

-

Pelobiotech

-

4titude

-

Corning Incorporated

-

Akron Biotech

-

Avacta Life Sciences Limited

-

Vericel Corporation

-

NuVasive, Inc.

-

Allergan

Recent Industry Developments

-

Feb 12, 2026 — StimLabs / Geistlich: Announced FDA 510(k) clearance for DermaForm™, a collagen scaffold particulate wound-care device for managing chronic and acute wounds. The update positioned it as a key portfolio and commercialization milestone.

-

Feb 3, 2026 — Geistlich: Announced FDA 510(k) clearance for its particulate collagen to be commercialized as DermaForm™ via StimLabs in the U.S. The company also highlighted an expanded partnership with a planned market launch timeline.

-

Jan 12, 2026 — StimLabs / Geistlich: Announced an expanded partnership to co-develop a new regenerative wound-care product, with launch targeted for the coming quarters. The companies emphasized combining R&D capability with commercial execution.

-

Oct 20, 2025 — REPROCELL: Announced the launch of Alvetex® Advanced, a next-generation 3D cell culture plasticware platform building on its Alvetex scaffold. The release emphasized improved culture flexibility, assay compatibility, and reproducibility for bioengineered tissue models.

-

Sep 8, 2025 — NurExone Biologic: Announced a U.S. patent allowance covering its exosome manufacturing process, including a 3D scaffold + shear-stress bioreactor concept. The company framed this as strengthening scalable production and clinical/commercial supply readiness.

-

Jul 8, 2025 — GeniPhys: Announced FDA 510(k) clearance for Collymer Self-Assembling Scaffold (SAS) for wound management. The company positioned the clearance as a step toward commercialization of its collagen-based scaffold technology.

-

Jun 23, 2025 — Carisma Therapeutics / OrthoCellix: Announced a definitive merger agreement to create an orthopedic regenerative cell-therapy company. The communication highlighted a platform combining a fortified 3D scaffold with proprietary bioprocessing to produce cartilage implants.

-

Mar 20, 2025 — BD: Announced a milestone in its PMA clinical trial evaluating GalaFLEX LITE™ Scaffold for breast implant revision surgery. The update emphasized progress toward regulatory approval for a breast indication.

-

Mar 19, 2025 — PHC / Cyfuse: Announced a 3D cell product production approach combining Bio 3D printing constructs with in-line monitoring during cultivation. The companies stated they will extend this into next-generation circulation cell-culture systems for more stable manufacturing.

-

Mar 6, 2025 — Atreon Orthopedics: Announced FDA 510(k) clearance expanding ROTIUM® Bioresorbable Wick indications to all tendon repairs. The company described ROTIUM as a fully resorbable synthetic nanofiber scaffold intended to promote remodeling and strengthen repairs.

-

Feb 20, 2025 — Atreon Orthopedics: Announced FDA 510(k) clearance and full market launch of BioCharge® Autobiologic Matrix for rotator cuff repair. The company positioned BioCharge as a resorbable synthetic scaffold designed to support healing biology and interface reinforcement.

What You Receive

• Global Scaffold Technology market size and growth projections (CAGR), 2024- 2034

• Impact of recent changes in geopolitical, economic, and trade policies on the demand and supply chain of Scaffold Technology.

• Scaffold Technology market size, share, and outlook across 5 regions and 27 countries, 2025- 2034.

• Scaffold Technology market size, CAGR, and Market Share of key products, applications, and end-user verticals, 2025- 2034.

• Short and long-term Scaffold Technology market trends, drivers, restraints, and opportunities.

• Porter’s Five Forces analysis, Technological developments in the Scaffold Technology market, Scaffold Technology supply chain analysis.

• Scaffold Technology trade analysis, Scaffold Technology market price analysis, Scaffold Technology Value Chain Analysis.

• Profiles of 5 leading companies in the industry- overview, key strategies, financials, and products.

• Latest Scaffold Technology market news and developments.

The Scaffold Technology Market international scenario is well established in the report with separate chapters on North America Scaffold Technology Market, Europe Scaffold Technology Market, Asia-Pacific Scaffold Technology Market, Middle East and Africa Scaffold Technology Market, and South and Central America Scaffold Technology Markets. These sections further fragment the regional Scaffold Technology market by type, application, end-user, and country.

FAQ's

The Global Scaffold Technology market is estimated to generate USD 1,973.9 Million in revenue in 2025

The Global Scaffold Technology market is expected to grow at a Compound Annual Growth Rate (CAGR) of 11.2% during the forecast period from 2025 to 2034.

The Scaffold Technology market is estimated to reach USD 5,292.4 Million by 2034.

Didn’t find what you’re looking for? TALK TO OUR ANALYST TEAM

Need something within your budget? NO WORRIES! WE GOT YOU COVERED!